Value investing is an investment strategy focused on buying stocks trading at a discount relative to their intrinsic or fair value.

Academic research indicates that value investing yields higher long-term returns compared to dividend and growth investing.

This workbook explores the realities of value investing and explains how to apply a value investing strategy to your portfolio. We’ll learn how to identify high-quality stocks with undervalued price tags using historical stock returns and market cycles.

What is Value Investing?

Value investing is an investment strategy based on the assumption that the stock market does not accurately value a company. Value investors believe they can make a healthy long-term profit by identifying profitable companies that the stock market undervalues.

It involves identifying companies with strong fundamentals that trade at a discount relative to their intrinsic value or future cash flows. By buying these stocks at a price lower than their intrinsic value, investors hope to eventually realize profits when the stock market accurately corrects and prices the stock.

Value investing is both a philosophy and an investment strategy. The philosophy is that an asset’s value is its most important characteristic. The strategy is that the market cannot properly value stocks, but well-informed investors can.

Value gurus like Warren Buffett believe most stocks are either overvalued or undervalued.

To determine the true value, value investors typically disregard the stock price and focus on the company as a whole. Value investors will examine a company’s sales data, financial reports, holdings, real estate, patents, intellectual property, research and development, and many other factors.

Value investors dream of finding a good stock that the market dramatically undervalues. Thus, many value investors are bargain hunters seeking the best value for their investment.

Many value investment strategies emphasize the intrinsic or real value of stocks. A popular value formula calculates the amount of cash a company generates. To determine the intrinsic value, investors examine a wide variety of metrics.

Value investment challenges many modern notions about capitalism. Many value investors reject the efficient market hypothesis, believing that markets are often inefficient and inaccurate.

Stock Rover 4.7/5⭐ : My Top Pick for Smart Investors

Investing In Stocks Can Be Complicated. Stock Rover Makes It Easy.

★

Growth Investing - with industry-leading

Research Reports ★

★ Value Investing - using Warren Buffett's Fair Value and Margin-of-Safety ★

★ Income Investing - rank by yield, growth, quality, and safety using 650 metrics ★

"I have been researching and investing in stocks for 20 years! I now manage all my long-term investments using Stock Rover." — Barry D. Moore, Founder: LiberatedStockTrader.com

Another popular belief of value investors is that investment industry professionals and the media cannot be trusted. These investors believe that the only reliable information about a company is its financial data. They ignore everything else.

A classic value-investing strategy seeks companies whose share prices are far below their intrinsic value per share. Followers of this strategy believe that the stock price will rise over time to reflect the company’s real value.

Most value investors focus on a company’s fundamentals, which means they examine financial reports, income statements, balance sheets, and other key financial documents. Many investors use financial data to help them estimate intrinsic value. Value investing can be confusing due to the numerous financial metrics and calculations.

The value gurus add to the confusion by emphasizing different numbers and factors. Warren Buffett emphasizes future free cash flow as one of the company’s most important criteria. However, Buffett’s teacher, Ben Graham, emphasized a company’s ability to consistently generate dividends for its investors.

Most value investors practice a buy-and-hold investment strategy. In buy-and-hold, a person purchases and holds a stock for an extended period.

The classic value investing idea is that you will not lose money on a stock that holds its intrinsic value. The usual value investing challenge is identifying low-priced, undervalued stocks with high intrinsic value.

Most value investors can be considered contrarians because they assume popular wisdom about stocks is wrong. A good way to think of value investing is that it believes the market is always wrong.

The Right Tools for Value Investing

My testing shows that the best value-investing stock screeners for Benjamin Graham & Warren Buffett portfolios are Stock Rover, Portfolio 123, TradingView, and TC2000.

Stock Rover is the best value investing stock screener overall because it features 650 screening metrics, including fair value and margin of safety, as well as Graham and Greenblatt calculations.

Portfolio 123 has 240 financial criteria, TC2000 has 90 fundamentals, and TradingView can scan for 48 financial metrics globally.

Academic Research Behind Value Investing

- “Value stocks have higher returns than growth stocks in markets around the world.” JSTOR Wiley Online Library

- “Two easily measured variables, size and book-to-market equity, combine to capture the cross-section of average stock returns.” JSTORIDEAS

- “Value strategies yield higher returns … because these strategies exploit the suboptimal behavior of the typical investor.” JSTOR Wiley Online Library

- “People tend to ‘overreact’ to unexpected and dramatic news events.” JSTOR+1

- “A simple accounting-based fundamental analysis strategy… can shift the distribution of returns earned by an investor.” JSTOR Ivey Business School

- “The evidence suggests that… value investing generates superior returns.” JSTORTaylor & Francis Online

Savings / Investing Goal Calculator

Calculate how much you need to save each month to reach a financial goal, how long it may take, and how investment returns can accelerate the journey.

Inputs

Results

Formula Used

Advanced Financial Goal Calculator for Saving and Investing

Ben Graham Value Investing

The British-American investor and economist Benjamin Graham is widely viewed as the father of value investing.

Graham first laid out his principles of value investing in his 1934 textbook Security Analysis. Graham popularized value investing with his 1949 classic, The Intelligent Investor, a seminal work on stock investing.

Both books are based on stock-investing lessons that Graham and others taught in a popular Columbia Business School course in New York City. The Intelligent Investor first outlined what is now widely viewed as value investing.

The Intelligent Investor teaches Graham’s most influential ideas, including Mr. Market and group investment. Mr. Market was Graham’s characterization of the stock market.

Graham described the stock market as a lunatic named “Mr. Market,” who sold stocks at insane prices. In Graham’s view, the key to making money was to catch Mr. Market when he was selling valuable stocks at low prices.

Graham’s approach is based on the theory that the market is inherently irrational. Mr. Market was Graham’s way of explaining that notion to ordinary people.

One of Graham’s primary teachings is that investors need to evaluate stocks for their ability to make money. Graham’s definition of a good company generates lots of cash. Graham’s definition of a good stock is equity that generates high dividends.

Graham believed that the ability to make money was the only criterion by which to judge stocks. His first rule of investing best sums up his philosophy. When faced with a new stock, Graham asked investors, “Does it make money?”

You want to be a successful stock investor but don't know where to start.

Learning stock market investing on your own can be overwhelming. There's so much information out there, and it's hard to know what's true and what's not.

Liberated Stock Trader Pro Investing Course

Our pro investing classes are the perfect way to learn stock investing. You will learn everything you need to know about financial analysis, charts, stock screening, and portfolio building so you can start building wealth today.

★ 16 Hours of Video Lessons + eBook ★

★ Complete Financial Analysis Lessons ★

★ 6 Proven Investing Strategies ★

★ Professional Grade Stock Chart Analysis Classes ★

Graham’s second rule of investing was to “see rule number one.” In Graham’s teaching, the ability to make money is the most important attribute of any investment.

Graham invented what he called the group approach to identify such stocks. In the group approach, you identify criteria for undervalued stocks and search for equities that meet those criteria.

Graham attracted attention for claiming that stocks picked by his group gained value at twice the rate of the Dow Jones Industrial Average. The Dow Jones Industrial Average was the most popular stock index in the 20th Century.

Graham was an active investor who worked on Wall Street for decades. Graham was openly critical of the stock market, most investors, and corporations.

Today, Graham is best known as the primary teacher of his most famous pupil, Warren Buffett. Buffett studied under Graham at Columbia Business School and worked at Graham’s company, the Graham-Newman Partnership, early in his career.

Graham’s influence extends far beyond amateur value investors. Many mutual funds employ Graham’s diversification strategies, group investment, portfolio management, and financial analysis in their stock picking.

The key criteria for a Graham value investment are that a company must be cheap and generate a lot of money. This simplicity is what makes Graham’s value investing so popular.

Many investment professionals, however, view Graham’s ideas as too limited for today’s complex markets.

Warren Buffett Value Investing

Warren Buffett is the world’s most successful and famous value investor for a good reason.

Buffett is widely admired because he is among the world’s richest people. Most of that fortune comes from stock in his company, Berkshire Hathaway (NYSE: BRK.B). Much of Berkshire Hathaway’s money comes from its stock holdings, which Buffett helps pick.

Buffett bases his value investing on Graham’s philosophy but employs different tactics and criteria. Unlike Graham, Buffett is willing to pay higher prices for companies he considers good.

Buffett will buy more expensive stocks that meet his criteria. His portfolio has often contained expensive stocks, including Apple (NASDAQ: AAPL).

Another difference between Warren and Graham is that Buffett will buy large amounts of what he considers good stocks. Buffett’s strategy is to concentrate his investment on moneymaking equities.

When Buffett analyzes a stock, he pays the most attention to its cash flow and assets. Buffett’s core belief is that good companies always have lots of cash.

One difference between Buffett’s approach and Graham’s is the Oracle of Omaha’s focus on growth. Buffett will pay extra for companies like Apple that have healthy growth rates.

Berkshire Hathaway will sell companies with slow growth. In recent years, Buffett sold much of his stake in Walmart (NYSE: WMT) because of that company’s low growth rate.

Another Buffett belief is that investors must maintain large cash holdings. Berkshire Hathaway made headlines for accumulating $122.38 billion in cash and short-term investments in the summer of 2019.

Buffett teaches that investors need lots of cash to take advantage of opportunities fast. Investors also need cash to cover emergency expenses and to borrow against them.

Like Graham, Buffett is a contrarian famous for his skepticism of the market, the media, investors, and the investment industry. Buffett dismisses investment fads, popular wisdom, professional fund managers, and new technologies.

In recent years, Buffett has become increasingly critical of the wealthy and the American political system. To encourage the rich to give back, Buffett pledged to give 99% of his fortune to charity.

Buffett is a celebrity who has achieved rock-star status among investors. CNN reports that more than 16,200 people attended Berkshire Hathaway’s carnival-like shareholders’ meeting in Omaha, Nebraska, in May 2019. One highlight of the meeting was a public question-and-answer session where Berkshire Hathaway stockholders could ask Buffett anything.

Buffett’s value investing combines Graham’s philosophy with a contrarian view of the markets and a cynical view of human nature. Buffett likes to tell people to buy companies so simple that “even somebody’s idiot nephew” can run them. The notion is that “somebody’s idiot nephew” will be in charge eventually.

Buffett’s value formula is hard to calculate manually because it emphasizes several divergent criteria.

Unlike most investors, Buffett emphasizes cash flow and growth rate over share price.

Buffett does not take many risks when investing. He invests in stable, simple businesses, including insurance, consumer goods, retail, finance, and media.

Buffett’s methods are not for everybody because they require time to generate profits, emphasizing long-term, stable profits. Too many people are focused on short-term trading to make money, which is much riskier. Many people, however, swear by Buffett and his investing wisdom.

Research: Value Investing vs. Growth vs. Index Fund Performance

Value investing, growth investing, and index funds are popular investment strategies with unique advantages and risks. This comprehensive analysis aims to compare these strategies based on their performance.

Value Investing Performance

Value investing’s performance can vary significantly. Some studies suggest that value stocks may outperform growth stocks during certain periods 1, while others indicate no superior performance over the national market index 2.

Growth Investing Performance

Several studies indicate that growth stocks have outperformed value stocks over the long term. However, there are periods where value stocks have outpaced growth investments.

Index Funds Performance

Index funds’ performance is directly tied to the market index they track. Hence, their success is dependent on overall market performance.

Recommendations for Investors

Investors should consider a balanced approach that incorporates elements from all three strategies. This can mean investing in value stocks with potential, growth stocks for high returns, and index funds for stability and diversification.

In conclusion, while each strategy has merits, the choice largely depends on individual investor goals, risk tolerance, and investment horizon.

Sources:

- When do value stocks outperform growth stocks? Investor sentiment and equity style rotation strategies

- Do value stocks earn higher returns than growth stocks in an emerging market? Evidence from the Istanbul Stock Exchange

- Growth stocks outperform value stocks over the long term

Can You Invest Like Warren Buffett?

Yes, Warren Buffett has been vocal about his investing principles over the years; even his daughter wrote a book called Buffettology about them.

We have distilled it all into our blockbuster article called:

Value Investing Concepts

Most value investors base their decisions on three basic concepts. Each concept is a big idea that underlies the value-investment philosophy.

Three major value investing concepts are:

Intrinsic Value

Intrinsic value is the price of a business calculated through fundamental analysis of a company’s assets and cash flows.

A classic formula for intrinsic value is the sum of a company’s assets’ market value and its cash flows. Buffett value investors ignore a company’s share price when valuing it.

Instead, Buffett values the companies he invests in as if he were buying the entire business for cash. Once these investors calculate intrinsic value, they compare it to the share price and market capitalization. If the intrinsic value is substantially higher than the market capitalization, you can consider the company a value investment.

Buffett arrives at an intrinsic value by studying financial numbers and researching a company’s business model and competitors. For instance, Berkshire Hathaway could compare a company’s products and sales to those of its competitors.

A simple definition of intrinsic value is the cash value of everything a company owns. A slightly more complex estimate will include cash flows or projected cash flows.

Most value investors use several methods of analysis to arrive at intrinsic value. There is no single best formula for intrinsic value. Instead, investors usually base intrinsic value on the calculation that best fits their belief of what makes a great company.

Margin of Safety

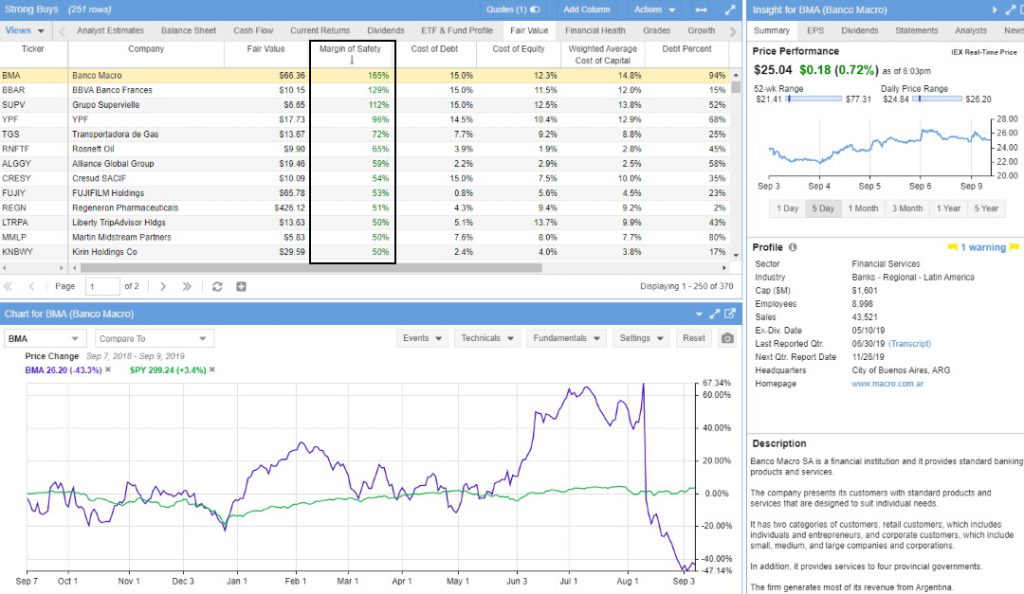

The margin of safety is the difference between a company’s share price and its intrinsic value.

In classic value-investing theory, the margin of safety is the level of risk an investor can live with. The margin of safety estimates the risk a stock buyer takes.

Warren Buffett describes the Margin of Safety like this:

“If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety. So, the more vulnerable the business is, assuming you still want to invest in it, the larger the margin of safety you’d need. If you’re driving a truck across a bridge that says it holds 10,000 pounds and you’ve got a 9,800-pound vehicle, if the bridge is 6 inches above the crevice it covers, you may feel okay, but if it’s over the Grand Canyon, you may feel you want a little larger margin of safety…”

The Margin of Safety is the percentage difference between a company’s Fair Value and stock price. This is the most significant valuation metric as it is the final output of a detailed discounted cash flow analysis.

A person who pays $300 per share for a company with a low intrinsic value of $200 is taking a big risk. Someone who pays $25 per share for a company with a high intrinsic value of $50 is taking much lower risk.

In this case, the Margin of Safety is 50%.

Get Stock Rover – The Best Software for U.S. Value & Growth Investors

The Margin of Safety Calculation

Margin of Safety = (Intrinsic Value Per Share – Stock Price) / Intrinsic Value Per Share.

Margin of Safety: (50-25)/50 = 50%

Another name for the margin of safety is the break-even analysis, which measures the share price at which you can profit from a stock.

Ben Graham and David Dodd created the term “margin of safety” in Security Analysis. Today, the Margin of Safety is one of the key concepts of value investing.

All value investors need to understand that the margin of safety is only an estimate of a stock’s risk and profit potential. Fundamental analysis cannot estimate many risks, including politics, regulatory actions, technological developments, natural disasters, popular opinion, and market moves.

The margin of safety you use is the level of risk you are comfortable with. If you are risk-averse, you will want a high margin of safety. A risk-taker, however, could prefer a low margin of safety.

Fundamental Analysis

They call the most common method value investors use to value a company “fundamental analysis.”

Classic fundamental analysts examine the qualitative and quantitative factors surrounding a company. Those factors can include economic conditions, financial conditions, market conditions, the political and regulatory environments, technology, and the industry’s overall state.

Fundamental analysis seeks to assess a company’s risk profile and its capacity to generate profits. Both value and growth investors use fundamental analysis.

Value investors focus on a company’s ability to make money. Growth investors look at a company’s capacity for future growth and stock price appreciation. A value investor could look at the company’s cash flow, while a growth investor will examine its research and development, sales growth, and earnings per share (EPS) growth.

To understand value investing, you need to understand fundamental analysis, intrinsic value, and margin of safety. Not all value investors use these concepts. Buffett will purchase stocks he likes, even if the market price exceeds the fair value margin.

Investors need to understand that these concepts are theoretical guidelines and not concrete rules. Many stocks will make money but violate some value-investing concepts.

9 Ways to Find Value Stocks

There is no universally best method of valuing a company in value investing. Value investors, instead, use a variety of valuation methods.

Some popular methods for valuing a company in the fundamental analysis are listed next.

Book Value

To a classical value investor, book value appraises all a company’s assets. A good definition of book value is the price the company can sell it for in cash now. Book value assets include real estate, equipment, inventory, accounts receivable, raw materials, investments, cash assets, intellectual property rights, patents, etc. Disney’s (NYSE: DIS) book value includes the land on which its studios and theme parks sit. Disney’s book value also includes its vast library of films, TV shows, and all the characters and stories Disney owns.

Tangible Value

Tangible value is the potential value that investors can easily calculate. A good example is the market price for equipment or real estate.

Tangible Book Value

Tangible book value, or tangible equity, measures a company’s value excluding all intangible assets. It could include only physical assets and cash investments.

Intangible Value

A company’s intangible value is the money it could theoretically make from its assets. Intangible assets can include patents, trademarks, business plans, strategies, customer goodwill, fictional characters (e.g., Disney & Marvel), franchises, and research and development capabilities. A good rule of thumb is that an asset is intangible if there is no guarantee it will make money.

Enterprise Value

Enterprise value is the company’s total value, including market capitalization. It is the price another company could pay for a corporation. A classic formula to calculate enterprise value is market capitalization plus assets plus cash and equivalents minus debt.

Franchise Value

The franchise value is a company’s name or reputation. The idea is that a good name or reputation will increase a company’s value, sales, and cash flow. Apple has a high franchise value because of its reputation for making dependable, innovative, and high-quality products. This enables Apple to charge higher prices and sustain high profit margins while maintaining a loyal customer base.

Dividend Value

The dividend value or yield is the amount investors can earn from a company’s dividends. They usually calculate dividend value by subtracting the annualized payout from the share price. The annualized payout is the dividends generated by a share of stock in the past year.

Negative Enterprise Value

A company has a negative enterprise value when the cash on the balance sheet exceeds its market capitalization and debts. Value investors look for negative enterprise value because it indicates Mr. Market is undervaluing a company.

Net Current Asset Value Per Share (NCAVPS)

NCAVPS was one of Benjamin Graham’s tools for valuing a stock. You calculate the NCAVPS by subtracting a company’s total liabilities from its current assets. Graham considers preferred stock a liability. The idea is to learn how much money a company will have left after selling all its cash assets and paying all its obligations.

There is no perfect method for valuing a company. Most value investors have a favorite method, but their choices often reflect preferences or prejudices rather than results.

It is best to test and use all the methods and find the one you are most comfortable with.

Value Investing Strategy

Value investing is ultimately a matter of strategy. Thus, we can think of value-investment masters like Buffett and Graham as strategists.

Buffett’s strategy is to look for growing, high-quality companies that generate large amounts of cash. The Graham strategy is to seek stable, low-priced companies that generate lots of cash.

Graham and Buffett ultimately diverged a little in their strategies. Graham’s strategy was diversification, which involved buying several stable stocks to create a high margin of safety.

Buffett uses a concentration strategy in which Berkshire Hathaway (NYSE: BRK.B) buys as much of a good company’s stock as possible, preferably to own the company outright. Buffett considers cash flow, growth, and the margin of safety important. Graham considered the margin of safety the most important aspect of value investing.

In Buffett’s strategy, cash flow is a tool for growth. A cash-rich company can afford to upgrade its technology, expand into new markets, develop new products, increase marketing, and borrow large amounts of money. Thus, a cash-rich company is more likely to grow.

One of Buffett’s conclusions is that a company is unsafe unless it grows. To ensure growth and cash flow, Buffett designed the strategy of buying growing companies.

Graham designed his strategy to create a wide margin of safety by spreading the investment over many stocks. Buffett’s strategy generates cash by concentrating investment in cash-rich companies.

Dividend Value Strategy

Graham and Buffett use dividend value because it ensures a steady cash flow. The difference is that they use dividend values differently.

Graham strategists view a high dividend yield as a means of increasing the margin of safety, while Buffett strategists see it as cash they can use to fuel future growth.

Franchise value is key to the Buffett strategy, but ignored in the Graham strategy. Buffett will pay more for companies with strong franchises because he believes they generate more revenue.

Graham strategists view a company’s share price as a more important metric than its franchise value. In their worldview, the share price can tell whether a company is overpriced or underpriced.

Graham strategists consider the share price a measure of the margin of safety. In this world, the higher the share price, the smaller the margin of safety.

Under the Buffett worldview, the share price has no relation to the company’s true value. Buffett considers the franchise value a better indicator of a company’s true value. In Buffett’s world, the higher the franchise value, the more money the company can make.

The Strategy of Market Irrationality

Both Buffett’s and Graham’s strategies try to capitalize on market irrationality.

Graham’s strategy is based on the idea that the market often grossly underprices good stocks. A popular view of Graham investors is that investors pay less for stocks they dislike and boring stocks.

Another of Graham’s ideas is that investors pay more for stocks they like, even if they make less money. Modern value investors use the slang of sexy and unsexy stocks.

Value investors believe people pay more for attractive, fashionable, or “sexy” stocks. Therefore, many value investors look closely at unattractive, boring, unfashionable, or “unsexy” stocks. These people seek good stocks that the market does not appreciate.

For instance, a Graham value investor could buy an oil company instead of a tech stock. The oil company is old-fashioned, boring, and offensive to some people, but it makes money. The tech company is attractive and flashy, but it could make no money.

Market irrationality partially explains Graham’s question: “Does it make money?” Graham investors often look at the balance sheet and ignore the business.

Buffett thinks that popular opinion and the media create market irrationality. Buffett watches the news and looks for bad news about good companies.

The idea behind this strategy is that news reporting is usually shallow, superficial, and concentrated on one aspect of a company’s business. Buffett will sometimes buy companies after a well-publicized scandal.

Despite a scandal at that company, Berkshire Hathaway (NYSE: BRK.B) kept large holdings of the banking giant Bank of America (NYSE: BAC). The public turned on Bank of America after news reports alleged some employees were writing fake loans to get commissions.

Buffett kept Bank of America because the bad loans stemmed from a single small part of its business. Buffett hoped the bad news about Bank of America would fade, but the company could continue to make money.

Another key idea in Buffett’s market-irrationality strategy is that the media does a poor job of reporting on companies. Buffett bets that most financial news about companies will be inaccurate, limited, short-sighted, biased, and incomplete.

Buffett tries to capitalize on that lack of information by having more information than the rest of the market. Buffett reads financial reports rather than newspapers and blogs because he believes financial data gives him an edge over other investors.

Buffett assumes that most investors value companies poorly because they rely upon inaccurate media reports. Uncle Warren’s strategy is to seek more accurate information and base his decisions on it.

Diversification Strategy

The most popular value investing strategy is diversification, designed to create a high margin of safety.

Diversified investors assume most people make poor stock choices. The diversified investor seeks to counteract poor stock choices by buying a range of stocks that meet his criteria.

A diversified investor seeking dividend income will buy high-dividend-yield stocks in several industries to create safer cash flow. A diversified investor seeking franchise value will buy stocks in companies with high franchise value.

Buffett buys a variety of growing cash-rich companies to create high cash flow. Buffett hopes that Berkshire Hathaway (NYSE: BRK.B) will always generate some cash from its many businesses.

Understanding the strategy is the key to learning value investing. All good value investors are good strategists. The ultimate goal of a successful value investor is to design and implement a value-investing strategy.

Simplifying Value Investing

The truth is that today, value investing and dividend investing are a lot easier due to the power of the internet and web-based service providers that do the hard work and calculations for you.

Excel spreadsheet calculations are a thing of the past, as serious computing power enables you to scan an entire stock market for your exact value investing criteria in seconds when you find potential new investments.

From our thousands of hours of testing, there is only one choice for value investors: Stock Rover, winner of our Best Value Investing Stock Screener Review, and joint winner of our Top 10 Best Stock Analysis Software Review.

Value Investing eBook/PDF Download

Click this link to download and open the Value Investing, Strategy & Screening Guide eBook PDF.

FAQ

What software is best for value investors?

The best software for value investing is Stock Rover. I use Stock Rover for all my value investing strategy development, research backtesting, and portfolio management. My original research on growth and value strategies is all conducted with Stock Rover.

Does value investing beat the market?

Yes, research by Fama & French revealed that value investing tends to outperform the market over the long term. However, it's important to note that a value investing strategy may underperform in some years.

Does value investing still work?

Yes, despite periods of underperformance, value investing continues to be a viable strategy. It requires patience and rigorous financial analysis using Stock Rover but has shown potential for high returns over time.

How does value investing work?

Value investing involves identifying stocks that are undervalued compared to their intrinsic value. This requires comprehensive financial analysis and the patience to wait for these stocks to appreciate.

How to do value investing?

To practice value investing, you must screen for value stocks, understand financial statements, identify undervalued stocks, and wait for the market to realize their true value.

How do you find good value investing stocks?

Finding value stocks requires a deep dive into a company's financials. Look for low price-to-earnings (P/E) ratios, strong dividend yields, a high margin of safety, and solid cash flows.

What software is best for margin of safety and fair value?

Stock Rover is the best software for managing value and growth investing using criteria like margin of safety, intrinsic value, and fair value; it is the complete solution for long-term investors.

Is systematic value investing dead?

No, systematic value investing is not dead. There may be periods where it underperforms, but it's a proven strategy for long-term investing, as proven in Eugene Fama's research.

Is value investing still relevant?

Yes, value investing remains relevant. Despite short-term fluctuations and falling in and out of fashion, it still offers a disciplined, systematic approach that can yield solid returns over time.

Is value investing worth it?

The worthiness of value investing depends on individual investor goals and risk tolerance. It can be very rewarding for those who are patient and willing to conduct thorough financial analysis.

Is value or growth investing better?

Neither strategy is inherently better; both have their merits and drawbacks. While growth stocks might excel in bull markets, value stocks outperform during bear markets and economic recessions.

What is a value trap in investing?

A value trap is a stock that appears to be cheap but is actually fundamentally poor. It's a risk for value investors who might be lured by the seemingly undervalued price.

What is relative value investing?

Relative value investing is a strategy that seeks to identify assets and investments where the relative prices of related securities are out of sync to take advantage of any mispricings. It often involves buying assets that are undervalued or selling those that are overvalued.

Why does value investing work?

Value investing works because it capitalizes on market overreactions, buying stocks when they're undervalued and selling when they reach their intrinsic value. It is the ultimate buy low, sell high strategy.

Did Eugene Fama support value investing?

Yes, Eugene Fama was a firm supporter of value investing. In his 1992 paper discussing "the efficient market hypothesis," he concluded that "value stocks tend to outperform growth stocks in the long run." He further argued that these outperformance results may be because markets overreact to new information and follow trends, leading to mispriced securities.

Do a lot of people follow value investing?

Yes, many people follow value investing. Warren Buffett is one of the most famous proponents of value investing, and his strategies have produced massive returns for himself and his investors over time. In addition, numerous hedge and mutual funds utilize value investing to generate consistent returns.

What makes value investing so attractive?

Value investing appeals to investors because it is a low-risk strategy that seeks to identify stocks that are trading at a discount and take advantage of them. If the stock does not perform as expected, the investor can easily exit their position without taking too much of a loss. In addition, value investing allows investors to purchase stocks with strong fundamentals before the market realizes.

Does Buffett still think value investing works?

Yes, Warren Buffett is still a strong believer in value investing. He often cites Benjamin Graham's "intelligent investor" principles as the foundation of his investment philosophy. He has said that he does not invest in anything he does not believe to be undervalued.

Does value investing still make sense?

Yes, for patient investors who understand financial analysis, value investing can make a lot of sense and potentially offer high returns.

Does Value Investing Beat the Market?

Yes, value investing beats the market, but only over long periods of time. Warren Buffett's value investing company Berkshire Hathaway has returned an average 23% per year over the last 30 years. The S&P 500, has averaged 9% year-on-year.