A stock market crash feels like chaos when you’re living through it. Prices drop quickly, headlines turn scary, and it’s easy to believe that “everything is broken.” But for long-term investors, crashes can become opportunities—if you have a plan before the panic starts. This lesson explains that plan in simple terms: how to reduce damage, how to keep your confidence, and how to use cash and dollar-cost averaging to position yourself for the recovery.

The goal is not to “predict the next crash.” The goal is to make sure a crash doesn’t permanently derail your investing journey—and to give you a realistic way to benefit from lower prices without gambling.

What Happens in a Stock Market Crash (and Why It’s Not the End)

A crash is a rapid, significant decline in many stocks simultaneously. It usually occurs when uncertainty spikes—about the economy, interest rates, credit conditions, geopolitics, or corporate earnings. In that moment, fear spreads faster than facts.

Two things can be true simultaneously:

- Prices can overshoot to the downside (even for good companies).

- Some businesses are severely weakened and may take a long time to recover.

That’s why a crash is not a “buy everything blindly” moment. It’s a selective opportunity for investors who can stay calm, preserve capital, and deploy money when the odds improve.

The First Rule of Crash-Proof Investing: Don’t Rely on One Decision

Most beginners think investing is about making one perfect decision: “When should I buy?” But crashes teach a better lesson: investing is safer when you spread decisions over time and keep flexibility.

That flexibility comes from two tools:

- Dollar-cost averaging (DCA): investing gradually instead of all at once.

- Cash as a position: not being fully invested all the time, so you can act when prices are attractive.

These tools reduce the risk of poor timing, lower stress, and increase your ability to leverage extreme fear.

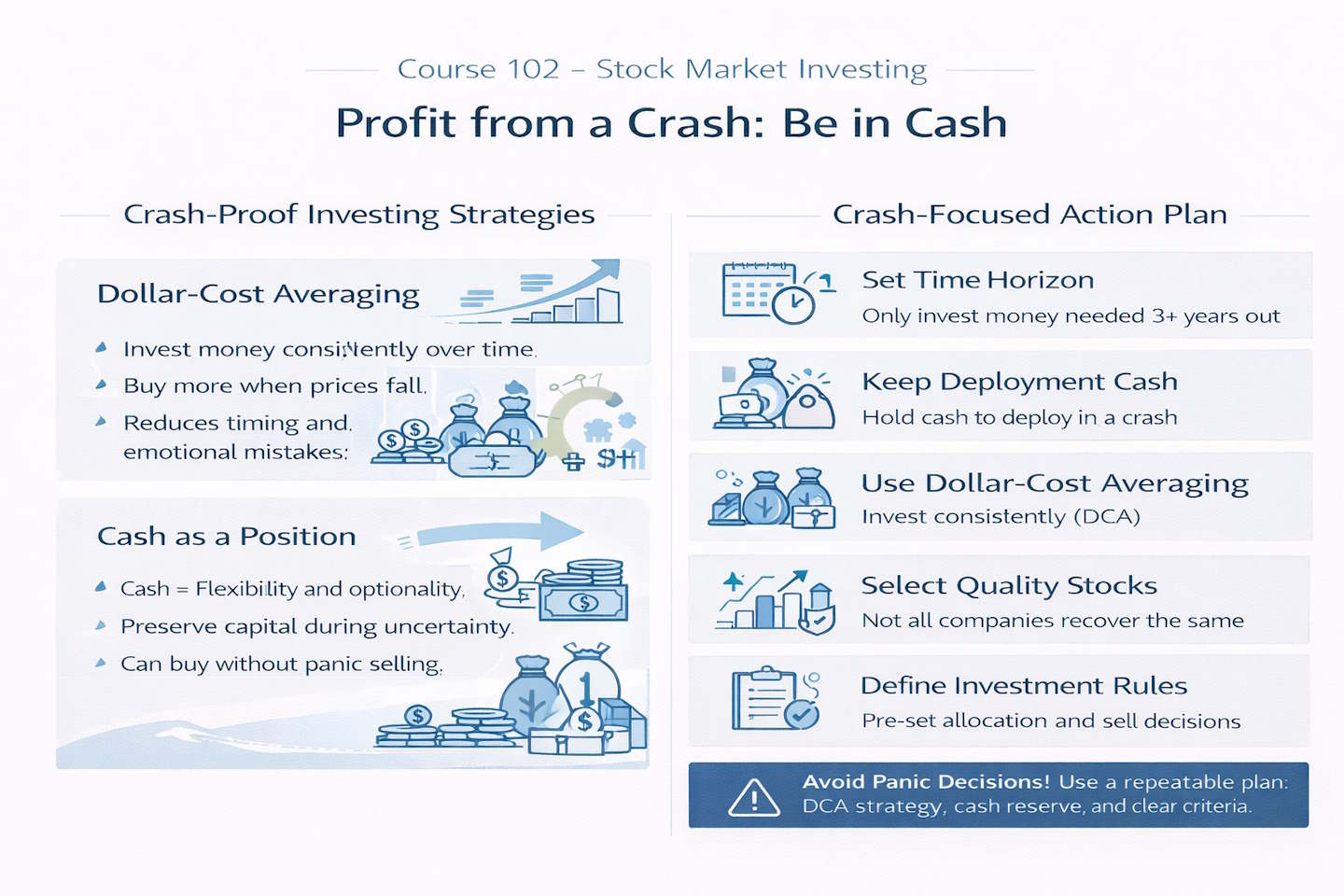

Dollar-Cost Averaging: Your Anti-Panic Strategy

Dollar-cost averaging (DCA) simply means you invest a fixed amount regularly (e.g., monthly) rather than investing all your money at once. The key benefit is behavioral and mathematical:

- If prices fall after you begin, your next purchases buy more shares at lower prices.

- If prices rise, you still participate—just with fewer shares bought at higher prices.

DCA is not about “beating the market.” It’s about reducing regret and avoiding the trap of trying to time a crash perfectly.

Why DCA helps specifically during crash fears

If you invest everything today and a crash happens next month, you’ll feel immediate pain—and many beginners panic-sell. DCA reduces that emotional shock because only part of your capital was exposed early.

A simple DCA example (beginner-friendly)

Imagine you have €1,000 to invest.

- Lump sum approach: invest €1,000 today.

- DCA approach: invest €100 per month for 10 months.

If markets drop in month 3, the DCA approach means you continue buying at discounted prices through months 4–10. It’s a built-in way to “buy more when it’s cheaper,” without needing courage at the worst moment.

The Second Tool: Cash Is Not “Doing Nothing”

Many beginners think being in cash is “missing out.” But cash is not a failure—it’s a strategic position. Cash gives you:

- optionality (you can buy when the value appears),

- safety (you reduce drawdown),

- and emotional control (you’re less likely to panic).

Independent investors have an advantage that institutions often don’t. Large funds frequently must remain mostly invested due to mandates and investor expectations. As an individual, you can choose to reduce exposure and hold cash when conditions become unusually risky.

This is not an argument to “stay in cash forever.” It’s an argument to treat cash like a tool—something you can use tactically when risk is elevated, and prices are unattractive.

Your Default Position: Why “Cash First” Improves Decision Quality

A useful mental model is:

Cash is the default. You earn the right to take risk.

From that default, you decide when to allocate to stocks based on your strategy and risk signals—not based on hype, fear, or social pressure. There is no shame in being in cash, especially during serious bear phases, because capital preservation keeps you alive for the next opportunity.

This is where beginners often misunderstand investing. They assume investing is only about maximizing returns. But long-term success is also about avoiding catastrophic mistakes. A large loss doesn’t just hurt emotionally—it changes the math.

The Math of Losses: Why Big Drawdowns Are So Hard to Recover From

Here’s a critical truth that every investor should internalize:

- If you lose 50%, you need a 100% gain to break even.

That’s not a motivational quote; it’s arithmetic. It illustrates this with an example of a stock dropping from $10 to $5, then returning to $10.

This is why “just hold and hope” can be destructive when the drawdown is large. Even if the stock eventually recovers, you may waste years just getting back to where you started—while also enduring stress that often causes bad decisions.

Two Crash Approaches: The Difference Between Hoping and Planning

The lesson provides two contrasting strategies. Let’s translate the logic into a clearer beginner framework.

2 Examples of Stock Market Crash Strategies

Strategy A: Hold and hope (common, emotionally comfortable, often inefficient)

Stock A – you BUY 100 shares @ $10 per share = $1,000 investment

Stock A – Drops to $5 per share (50% loss) = your investment is now worth $500

Stock A – Moves back to $10 per share.

This stock will need to return to $10 for your investment to recover, meaning you would need to make a 100% profit to break even.

This approach feels safe because you “didn’t do anything wrong.” But it can be costly because it ignores capital efficiency and risk control.

Strategy B: Risk-managed exit + patient re-entry (uncomfortable, often more effective)

Stock A – Bought 100 shares @ $10 per share = $1,000 investment

Stock A – Drops to $8.50 per share = you SELL and take the loss of 15% – investment value now $850 – you stay in cash.

Stock A – Drops to $5 – you BUY 170 shares @ $5 – invest your $850 back into the stock – investment value $850

Stock A – Increases to $10 – you SELL 170 shares @ $10 = $1700. This is a 70% Profit.

This illustrates that by exiting earlier and buying more shares at lower prices, you can potentially recover faster and even end with a meaningful profit—because you avoided the deepest part of the drawdown and used cash to buy when value was higher.

What to Do During a Crash: A Step-by-Step Checklist

Here is a beginner-friendly crash plan that aligns with the lesson’s spirit without requiring advanced trading skills.

1) Decide your time horizon first

- If you need the money within 1–3 years, it should not be in volatile stocks.

- If you’re investing for 10+ years, crashes are part of the path.

2) Keep a “deployment reserve.”

Hold some cash (or near-cash) that you can deploy during extreme fear. The amount depends on your risk tolerance. The key is that cash enables you to act when the market offers bargains.

3) Use DCA for consistency

Even in scary markets, consistent investing prevents “analysis paralysis.” DCA is your default engine.

4) Be selective—don’t assume all companies recover equally

Some stocks rebound quickly while others take years.

So your job is to focus on quality: durable businesses, strong balance sheets, and products people still need.

5) Protect capital with rules, not emotions

If you use stop-loss rules or risk limits, define them before the crash. If you don’t want to trade, at least use allocation rules (e.g., maximum percentage in any one stock, maximum exposure to any one sector).

The Big Lesson: Cash Turns Fear into Opportunity

Don’t sit and hope—preserve capital and wait for better days.

For beginners, that becomes a mature investing mindset:

- When markets are euphoric, don’t assume the party lasts forever.

- When markets crash, don’t assume the world ends tomorrow.

- Keep a plan that lets you keep buying (DCA) and keep flexibility (cash).

That combination—steady investing + optionality—is how you survive crashes and benefit from recoveries without needing to be a professional trader.

A stock market crash can be a buying opportunity for investors who are patient and have a long-term outlook. During a stock market crash, stock prices fall dramatically, often giving investors a chance to buy stocks at a discount. However, not all stocks will be affected equally by a stock market crash.

Beat The Market, Avoid Crashes & Lower Your Risks

Nobody wants to see their hard-earned money disappear in a stock market crash.

Over the past century, the US stock market has had 6 major crashes that have caused investors to lose trillions of dollars.

The MOSES Index ETF Investing Strategy will help you minimize the impact of major stock market crashes. MOSES will alert you before the next crash happens so you can protect your portfolio. You will also know when the bear market is over and the new rally begins so you can start investing again.

MOSES Helps You Secure & Grow Your Biggest Investments

★ 3 Index ETF Strategies ★

★ Outperforms the NASDAQ 100, S&P500 & Russell 3000 ★

★ Beats the DAX, CAC40 & EURO STOXX Indices ★

★ Buy & Sell Signals Generated ★

MOSES Helps You Sleep Better At Night Knowing You Are Prepared For Future Disasters

DO NOT SIT AND HOPE – TAKE ACTION TO PRESERVE YOUR CAPITAL AND WAIT FOR BETTER DAYS.

There is no shame in being in cash.

Most experienced investors trading their accounts use this to their advantage. Knowing everything about technical and fundamental analysis will not help if you refuse to move to cash when the market enters a serious bear phase. Money management and capital preservation are critical. If you risk too much and lose too much, you will not have enough money to invest when the going gets good.

The more you lose in a downturn, the more you must make on the upturn to break even.

Now you know what to do.

In example 1, you faced the stress of holding a losing trade for an extended period and ending up with no profit.

In example 2, you took your losses on the chin early. However, you waited patiently for the right time to re-enter, recoup your early loss, and realize a significant profit.

Class Questions & Answers

What is dollar-cost averaging (DCA), and why is it useful during crash fears?

Dollar-cost averaging means investing a fixed amount regularly over time instead of investing all at once. It helps during market crashes: if prices fall, your future contributions buy more shares at lower prices, reducing timing risk and emotional stress.

Why can holding cash be an advantage during a market crash?

Cash gives you flexibility (optionality). During a crash, prices can become attractive, and having cash allows you to buy when opportunities appear instead of being forced to watch from the sidelines or sell other holdings at bad prices.

Why is a 50% loss so damaging to long-term returns?

Because losses compound against you: if you lose 50%, you need a 100% gain to return to break-even. Large drawdowns make recovery mathematically harder and often trigger emotional mistakes.

What is the core difference between “hold and hope” and a risk-managed crash strategy?

“Hold and hope” accepts deep drawdowns and waits for a return to the buy price. A risk-managed strategy limits losses earlier, preserves cash, and then re-enters when the risk/reward improves—potentially recovering faster and more efficiently.

What is one practical rule a beginner can follow to avoid panic decisions in a crash?

Pre-commit to a simple process: keep investing gradually via DCA, keep a cash reserve for opportunities, and avoid making major “all-in/all-out” decisions based on headlines or one scary week in the market.