You want to get how the stock market really works—without all the noise or jargon.

The stock market is basically a system where investors buy and sell pieces of companies, creating a marketplace that mirrors business results, investor moods, and larger economic swings.

When you look at it as just organized trading of company ownership, the process starts to feel less intimidating and more manageable.

You’ll see how money moves between investors and companies, what actually drives stock prices, and how to use tools—like Stock Rover—to analyze performance before you put money in. Each idea builds on the last, so you can start connecting the dots between company earnings, market cycles, and your own financial plans.

Key Takeaways

- The stock market lets you buy and sell pieces of companies.

- Prices shift based on company results, investor behavior, and overall trends.

- You can use research tools to build a balanced, goal-focused investment plan.

What Is the Stock Market?

![What is the stock market [flow chart]](https://www.liberatedstocktrader.com/wp-content/uploads/2025/12/what-is-the-stock-market-flow-chart.jpg)

The stock market connects companies that want capital with investors looking to grow their money. Organized exchanges run the show, with shares trading every day and prices set by supply and demand.

Ownership in Companies and Shares

When you buy a share, you’re really buying a tiny slice of the company itself. Each share gives you a claim on part of the company’s assets and earnings. Public companies issue shares to raise money for new projects, R&D, or just to pay down debt.

Shares mainly fall into two categories: common and preferred. Common shares usually come with voting rights at shareholder meetings, while preferred shares often pay fixed dividends but don’t offer a vote.

You can track how shares perform using market data platforms like Stock Rover. These let you dig into revenue growth, profit margins, valuation ratios—details that help you decide if a stock matches your goals and risk appetite.

Major Stock Exchanges: NYSE and Nasdaq

The New York Stock Exchange (NYSE) and Nasdaq are the two biggest U.S. stock exchanges. NYSE, around since 1792, uses an auction model where human specialists and electronic systems match orders. Nasdaq, which started in 1971, is fully electronic—no trading floor at all.

NYSE lists big names like Coca-Cola or IBM. Nasdaq tends to feature more tech companies, like Apple and Microsoft. Both require companies to meet strict standards for size, governance, and financial reporting.

You can check out live market data, charts, and trading volumes for both using TradingView. It’s handy for comparing liquidity and volatility between the two.

The Role of Investors and Brokers

Investors provide the capital by buying shares, and brokers handle the actual trades on exchanges. You’ll need to open a brokerage account to place orders—these might be market, limit, or stop orders. Some brokers charge commissions, others make money on the spread, depending on their platform.

Big players like mutual funds and pension funds trade in massive volumes, so they move prices more than individuals. Most retail investors use online brokers with low fees and easy interfaces.

If you’re into short-term trading or want to automate things, tools like TrendSpider let you test strategies and set alerts. Always check trade costs, execution speed, and regulation before you settle on a broker.

How the Stock Market Works

You buy and sell shares on exchanges that match buyers and sellers instantly. Prices shift as investors react to company news, economic reports, or just plain market mood. Knowing how shares are issued, traded, and priced gives you a real edge as an investor.

Primary and Secondary Markets

Companies get their first big cash boost by issuing shares in the primary market. This usually happens through an initial public offering (IPO), where investors buy shares directly from the company. The money raised goes straight to the company for things like operations, debt, or expansion.

After the IPO, shares hit the secondary market, and investors trade with each other. The company doesn’t get any more money from these trades, but the price reflects what investors think the company will earn down the line.

You access the secondary market by opening a brokerage account. Online brokers route your orders to exchanges like NYSE or NASDAQ. Every trade just moves ownership from one investor to another.

| Market Type | Who Sells Shares | Who Receives Money | Example |

|---|---|---|---|

| Primary | Company | Company | IPO of a new tech firm |

| Secondary | Investor | Investor | Buying Apple shares on NASDAQ |

If you want to look up IPO stats or screen for undervalued companies, tools like Stock Rover make it easier to compare fundamentals and results quickly.

How Trades Are Executed

When you place an order with your broker, it shoots electronically to an exchange or market maker. The system matches your order with someone else’s. How fast your order fills depends on liquidity and the kind of order you use.

Common order types include:

- Market order: Buys or sells right away at whatever price’s available.

- Limit order: Sets a max (buy) or min (sell) price you’ll accept.

- Stop order: Turns into a market order after hitting a certain price.

Brokers often use smart routing to get you the best fill. Some charge small fees, some offer commission-free trades—it all depends on your account.

You can keep an eye on order flow and execution data using MetaStock or Benzinga Pro, both of which stream live market feeds and alerts for traders who want to stay on top of things.

Stock Prices and Supply and Demand

Stock prices move because of supply and demand. If more people want to buy than sell, prices go up. If sellers outnumber buyers, prices drop.

Earnings, interest rates, and investor confidence drive demand. Broader stuff, like GDP growth or inflation, also shifts market mood.

Short-term traders lean on technical analysis to spot price trends and entry points. TrendSpider automates charting and pattern spotting so you can test ideas before risking your cash.

Long-term investors pay more attention to fundamentals like revenue, margins, and debt. Mixing market data with company analysis helps you figure out if a stock’s really worth your money.

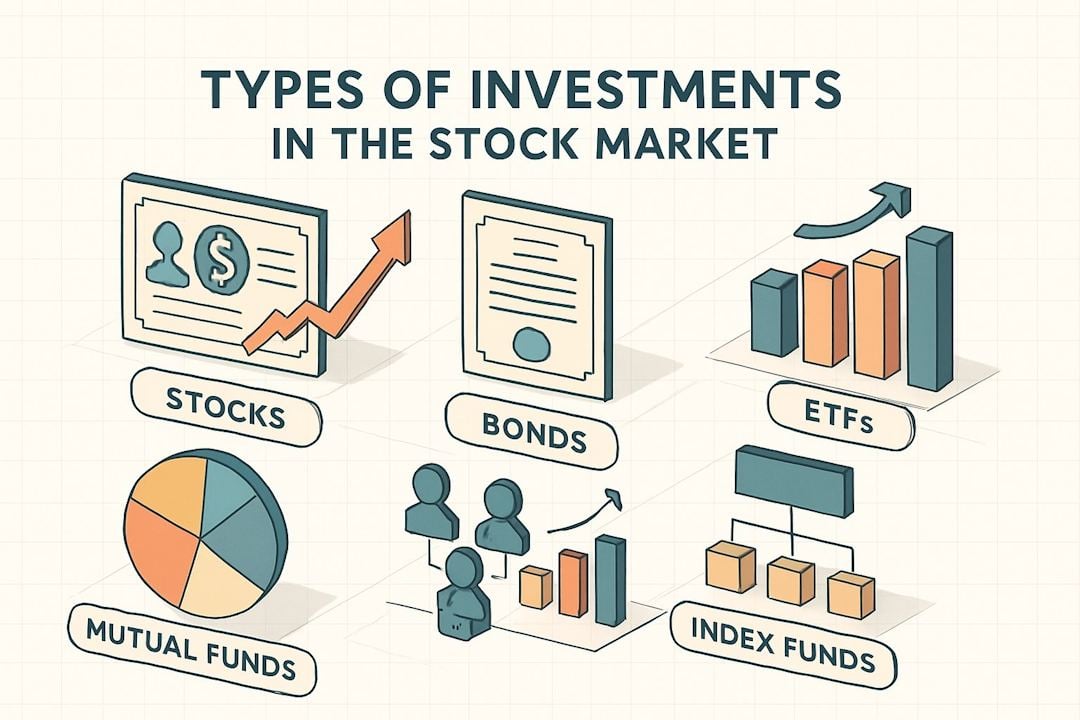

Types of Investments in the Stock Market

You can invest in a range of securities, each with its own risk, cost, and diversification level. Each option gives you different control, market exposure, and return potential. Knowing the basics helps you decide where you’re most comfortable putting your money.

Individual Stocks

When you buy individual stocks, you own a piece of a single company. If the share price rises or the company pays dividends, you make money. You also risk losing value if the business stumbles.

Stocks trade on exchanges like NYSE or NASDAQ. Prices shift daily based on earnings, economic news, and how investors feel about the market. You can track these moves using TradingView, which gives you live charts and technical indicators from around the world.

Owning individual stocks puts you in charge of your portfolio. You can zero in on specific sectors, like tech or healthcare, or pick companies that match your values. Building a balanced portfolio from scratch takes work, though—spread your bets across at least 15–20 companies to avoid putting all your eggs in one basket.

Exchange-Traded Funds (ETFs)

Exchange-Traded Funds (ETFs) are baskets of securities that trade like stocks. Each ETF tracks an index, sector, or asset class, such as the S&P 500 or emerging markets. You can buy and sell ETF shares all day at market prices.

ETFs give you instant diversification for a low cost. One share might cover hundreds of companies. They usually have lower expense ratios than mutual funds and no minimum investment, but you still pay brokerage commissions and face market swings.

You can screen ETFs by performance, holdings, and fees with Stock Rover, which helps you compare returns and risk. ETFs make sense when you want broad exposure without hand-picking individual stocks.

Index Funds and Mutual Funds

Index funds and mutual funds pool money from a bunch of investors to buy a range of securities. Index funds passively track a benchmark like the S&P 500, while mutual funds might have managers trying to beat the market.

Both offer diversification and simplicity. You own a piece of the fund, not the individual stocks. Returns depend on the fund’s holdings, minus fees.

Index funds usually cost less since there’s not much management involved. Actively managed mutual funds charge more, but sometimes they outperform in certain markets. You can read up on fund details and manager track records over at Seeking Alpha to find one that fits your goals and risk level.

Getting Started with Investing

You start by setting up the right tools, defining your financial goals, and learning the language investors use. Each step builds your base for making confident investment moves.

Opening a Brokerage Account

A brokerage account is your door to buying and selling stocks, ETFs, and bonds. You can set one up online in just a few minutes with firms like Fidelity, Charles Schwab, or Vanguard. Most will ask for ID, a way to fund the account, and a quick agreement to their terms.

Compare account types before you commit. Taxable accounts are flexible, while IRAs or Roth IRAs work for retirement savings. Look for low trading fees, platforms that actually make sense to use, and solid research tools.

| Key Feature | Why It Matters |

|---|---|

| Commissions | Lower costs mean you keep more of your gains. |

| Research Tools | Let you dig into stocks and funds before buying. |

| Account Protection | SIPC covers up to $500,000 in assets if something goes wrong. |

If you want to analyze charts or automate trades, TrendSpider can help you test your ideas before you risk real money. Start small, and get a feel for how the platform handles trades before going bigger.

Setting Financial Goals

Clear financial goals drive every investment decision. Figure out what you’re investing for—retirement, a house, or just building wealth. Set timeframes and targets, like saving $100,000 in 10 years or aiming for 6% annual returns.

Try the SMART method:

- Specific: Spell out what you want.

- Measurable: Track your progress with real numbers.

- Achievable: Make sure your goals fit your income and savings rate.

- Relevant: Tie goals to what actually matters in your life.

- Time-bound: Give yourself a deadline.

Short-term goals work best with safer stuff like bonds or cash. Long-term goals can handle more bumps, so equities or index funds might fit. Stock Rover helps you screen investments based on your risk and time frame. Check your goals once a year and tweak them as your situation changes.

Understanding Financial Jargon

Financial jargon can sound intimidating, but honestly, most of it just describes straightforward concepts. Equity? That’s just owning a piece of a company. Dividend is the profit a company pays out to shareholders. Market capitalization tells you how big a company is in terms of its total value. Once you get the hang of these basics, reading analyst reports or following market news feels a lot less overwhelming.

It helps if you keep a small glossary handy or stick to reliable sources like Seeking Alpha for definitions. Try to focus on the key ratios—P/E (Price-to-Earnings) and EPS (Earnings Per Share)—since these numbers help you figure out if a stock seems overpriced or like a bargain.

When you bump into a term you don’t know, pause and ask yourself: does this change how I’d look at risk or reward? Building up your financial vocabulary really cuts down on confusion and helps you act on facts instead of hunches.

Managing Risk and Building a Portfolio

Managing risk comes down to controlling how much of your money is at the mercy of market swings. You balance potential gains with the risk of loss by spreading your investments, holding on long enough to ride out volatility, and staying alert to how economic shifts and investor moods move prices.

Diversification Strategies

A diversified portfolio helps cushion the blow if one asset tanks. You can spread your money across different asset classes: stocks, bonds, cash, and so on. Inside each group, mix it up by sector, region, and company size.

| Asset Type | Typical Role | Example Allocation |

|---|---|---|

| Equities | Growth potential | 60% |

| Bonds | Income and stability | 30% |

| Cash/Alternatives | Liquidity and hedge | 10% |

Diversification really works when your assets don’t all move the same way at once. Government bonds, for example, often go up when stocks drop. If you use tools like Stock Rover, you can compare fundamentals across industries before you decide where to put your money.

Don’t go overboard, though—owning too many things can water down your returns and make managing your portfolio a headache. Check your mix every quarter and rebalance if you see allocations drifting more than 5% from your targets.

Long-Term Investing

Long-term investing means letting time do the heavy lifting. If you hold quality assets for at least five years, you give compounding and dividend reinvestment a real chance to grow your money.

You can manage risk by matching your investments to how long you plan to keep them. For goals less than three years away, lean on bonds or cash. If you’re saving for retirement or education ten years out, a heavier dose of stocks makes sense.

Stick with your plan and keep contributing, even when the market gets rough. Dollar-cost averaging—putting in a fixed amount at regular intervals—smooths out your purchase prices and helps you avoid knee-jerk reactions.

TradingView can help you see historical price trends and spot those long-term moves. Sometimes, patience really does beat trying to time every twist and turn.

Investor Sentiment and Economic Factors

Market prices shift based on both hard data and collective mood swings. Investor sentiment—whether it’s fear, hope, or confusion—can move prices faster than the fundamentals back up. Economic stats like GDP growth, inflation, and jobs data set the tone and steer asset values.

When the economy’s humming, investors usually take more risks, and stock prices tend to climb. During rough patches or recessions, defensive sectors such as utilities or healthcare usually hold up better.

Check on economic indicators every month and see how they line up with market moves. MetaStock offers real-time news feeds, so you can spot changes in sentiment before they hit your portfolio.

Keep a quick checklist:

- Track inflation and interest rates.

- Watch consumer confidence numbers.

- Adjust your exposure if the market’s mood swings to extremes.

Stay aware, and you’ll have a better shot at matching your portfolio to both the market and your own risk comfort zone.

Dividends, Retirement Accounts, and Next Steps

You can earn income from stocks via dividends and build long-term security through retirement accounts like a 401(k) or IRA. Each plays its own part in helping you reach financial stability and avoid depending on short-term gains.

Dividends and Income

A dividend is a cash payout or sometimes extra shares that a company gives to shareholders, usually from profits. You’ll get paid quarterly or annually, depending on the company’s rules. If you’re retired or just want reliable income, dividend-paying stocks can be a solid choice.

Dividend yield tells you the annual payout as a percentage of the stock price. For example, a $2 dividend on a $50 stock means a 4% yield. You can compare yields across sectors using Stock Rover, which lets you screen by payout ratio, growth history, and stability.

A lot of people use Dividend Reinvestment Plans (DRIPs) to automatically buy more shares with their dividends. This can help your returns snowball over time. Just remember, dividends in regular brokerage accounts are taxable, so keep track of your cost basis and your tax rate.

When you’re looking at dividend stocks, check the payout ratio (dividends divided by earnings). If it’s above 70%, the company might not have much room to grow or could cut payouts if things get rough. It’s usually better to stick with firms that have steady earnings and moderate payout ratios.

401(k) and IRA Basics

A 401(k) is a retirement plan your employer sponsors, letting you invest pre-tax income. Many employers match a chunk of what you put in, which is basically free money. You pick from mutual funds, index funds, or target-date funds inside your plan.

An IRA (Individual Retirement Account) works similarly but you set it up on your own. You can choose between a Traditional IRA (tax-deferred growth) or a Roth IRA (tax-free withdrawals in retirement). For 2025, you can put up to $23,000 into a 401(k) and $7,000 into an IRA, with higher limits if you’re over 50.

Keep your mix balanced—stocks, bonds, dividend payers—so you get both growth and income. Use TradingView to watch performance and test different allocations.

If your employer matches contributions, always put in enough to get the full match before investing elsewhere. After that, you can use your IRA for more investment options or lower-cost funds.

Lesson Review Questions

1. What is the basic role of the stock market?

The stock market connects companies that need capital with investors seeking returns. Companies issue shares—small ownership slices of the business—and investors buy and sell those shares to participate in the company’s potential profits.

2. Why do stock prices move up and down?

Stock prices move because of supply and demand combined with changes in how people view the company’s prospects. As new information appears—earnings, economic news, or company announcements—buyers and sellers adjust their expectations, and this constant re-pricing makes values change throughout the day.

3. What role do exchanges like the NYSE and NASDAQ play?

Public exchanges such as the NYSE and NASDAQ provide the marketplace where trades happen. Their electronic systems match buy and sell orders, ensuring that investors can quickly find a counterparty and that stock prices are set transparently based on all current bids and offers.