Bonds are the foundation of the global debt markets and a core building block of most long-term investment portfolios. While stocks represent ownership in a company, bonds represent a loan. When you buy a bond, you are lending money to a government, municipality, or corporation in exchange for regular interest payments and the promise to receive your original investment back at maturity.

Because bonds offer relatively predictable income and tend to be less volatile than stocks, they are especially important for risk-aware investors, retirees, and anyone who wants to balance growth with stability. Understanding how bonds work will help you make better decisions about diversification, risk management, and asset allocation across your entire portfolio.

In this lesson, you will learn what a bond is, how bonds pay interest, the many different types of bond investments available, the key risks and benefits, and how bonds can support your broader investing goals alongside stocks, ETFs, and money market instruments discussed in earlier lessons.

What Is a Bond?

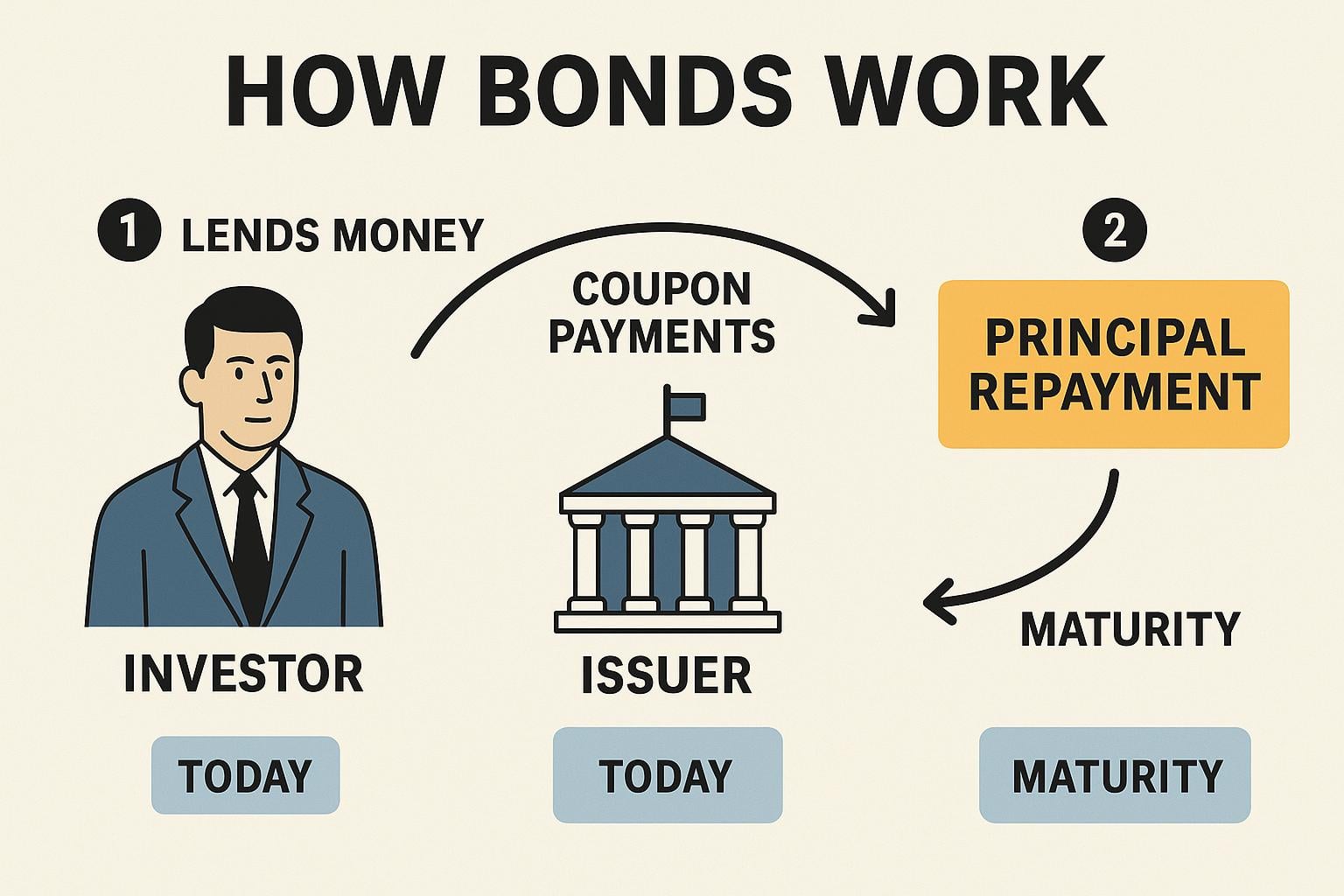

A bond is a formal agreement between an issuer and an investor. The issuer can be a government, municipality, or corporation that needs to borrow money. The investor is the lender who provides capital by purchasing the bond.

- The issuer promises to pay the investor regular interest (called the coupon).

- At the end of the bond’s life, called maturity, the issuer repays the principal or face value (for example, $1,000 per bond).

- The investor expects to receive both the coupon payments and the principal, assuming the issuer does not default.

Bond investors therefore focus on three key numbers:

- Face value: The amount repaid at maturity (commonly $1,000).

- Coupon rate: The interest rate stated on the bond (for example, 3% per year).

- Yield: The actual return based on the price you pay for the bond today.

Bond prices move inversely to market interest rates. When new bonds are issued at higher interest rates, existing bonds with lower coupons become less attractive and their prices fall; when rates drop, existing higher-coupon bonds rise in price.

How Do Bonds Work in Practice?

The word “bond” is often used generically for many types of debt securities, but the actual name depends on the length of time until maturity.

- Bills: Short-term debt, usually maturing in one year or less (sometimes up to five years). Example: U.S. Treasury bills (T-bills).

- Notes: Medium-term debt, typically maturing between two and ten years.

- Bonds: Long-term debt with maturities longer than ten or twelve years.

Consider a simple example. A government issues a 10-year bond with a face value of $1,000 and a coupon rate of 3% paid annually:

- You pay $1,000 to buy the bond at issuance.

- You receive $30 in interest every year for 10 years.

- At maturity, you receive your $1,000 back.

The interest rate the issuer must offer depends heavily on its credit quality. Strong, stable governments such as Germany can issue bonds at very low interest rates because investors see default risk as minimal. Countries with weaker finances or more political risk may have to pay much higher yields to entice investors to lend them money.

Why Invest in Bonds?

Bonds play several important roles in a diversified portfolio, especially when combined with equities and other asset classes covered earlier in this course.

- Income: Bonds pay regular interest, which can be valuable for retirees or anyone seeking predictable cash flow.

- Lower volatility: High-quality bonds are typically less volatile than stocks, helping smooth portfolio ups and downs.

- Capital preservation: When held to maturity and if the issuer does not default, you should receive your full principal back.

- Diversification: Bonds often behave differently from stocks, especially during market stress, improving overall risk management.

- Customizable risk levels: Investors can choose between conservative government bonds and higher-yield, higher-risk corporate or emerging-market bonds.

Certain bonds also provide tax advantages, such as municipal bonds whose interest may be exempt from local or national income taxes. We will revisit this later in the lesson.

For a broader view of how bonds fit next to stocks, ETFs, and cash as part of a long-term plan, revisit the lessons on managing financial risk and investing in money markets.

Types of Bond Investments

There are many flavors of bonds, each serving a slightly different purpose. The original article listed 26 categories; here they are grouped into a structured overview so you can see how they relate.

| Category | Bond Type | Key Features |

|---|---|---|

| Corporate | Corporate bonds | Issued by companies to fund expansion, R&D, or debt refinancing; risk and yield depend on company credit quality. |

| Corporate | High-yield (junk) bonds | Below investment grade; offer higher coupon rates to compensate for higher default risk. |

| Corporate | Convertible bonds | Can be converted into a specified number of the issuer’s common shares; offer upside if the stock performs well. |

| Corporate | Callable bonds | Issuer can redeem (call) the bond before maturity, usually when rates fall; reinvestment risk for investors. |

| Corporate | Puttable bonds | Investor has the right to sell the bond back to the issuer before maturity at a predetermined price. |

| Corporate | Floating-rate bonds | Coupons reset periodically based on a reference rate such as LIBOR or a central bank rate. |

| Corporate | Indexed bonds | Coupon or principal linked to an index (e.g., inflation index or stock index), providing some protection against inflation or market moves. |

| Corporate | Distressed bonds | Issued by companies in serious financial trouble; very high risk but potentially high reward for specialist investors. |

| Corporate | Private placement bonds | Sold directly to large institutions such as pension funds or insurers rather than to the public. |

| Government & Sovereign | Government bonds | General term for national government debt; considered relatively safe in developed markets. |

| Government & Sovereign | T-bills | Short-term U.S. Treasury securities with maturities of one year or less; sold at a discount and mature at face value. |

| Government & Sovereign | T-notes | U.S. Treasuries with maturities of two to ten years; pay semiannual coupons. |

| Government & Sovereign | T-bonds | Long-term U.S. Treasuries with maturities of 20 years or more; pay semiannual coupons. |

| Government & Sovereign | Emerging markets bonds | Issued by governments or corporations in emerging economies; higher yield but higher political and currency risk. |

| Government & Sovereign | Municipal bonds | Issued by states, cities, or local authorities to finance public projects; interest is often tax-exempt. |

| Government & Sovereign | Inflation-linked bonds (TIPS, I-bonds) | Principal is adjusted with inflation (e.g., Treasury Inflation-Protected Securities, Series I savings bonds), helping preserve real purchasing power. |

| Government & Sovereign | EE savings bonds | Government savings bonds that earn a fixed rate plus, in some cases, an additional inflation-linked component. |

| Structure & Coupon | Zero-coupon bonds | Pay no periodic interest; issued at a deep discount and mature at face value. All return comes at maturity. |

| Securitized | Asset-backed securities (ABS) | Backed by a pool of assets such as auto loans, credit card receivables, or student loans. |

| Securitized | Mortgage-backed securities (MBS) | Backed by pools of residential or commercial mortgages; cash flows depend on borrower payments. |

| Securitized | Collateralized debt obligations (CDOs) | Structured products backed by a bundle of other debts such as corporate bonds or loans. |

| Short-term Funding | Commercial paper | Unsecured, short-term promissory notes issued by large corporations to fund working capital. |

| Short-term Funding | Bills/notes/bonds by maturity | Generic terms describing loans of increasing length; short-term bills, medium-term notes, and longer-term bonds. |

| Government Inflation Products | Series I savings bonds | Savings bonds that combine a fixed rate with an inflation-adjusted rate based on the CPI. |

| Government Inflation Products | Treasury Inflation-Protected Securities (TIPS) | U.S. government bonds whose principal is adjusted for inflation, with interest paid on the inflation-adjusted principal. |

As a new investor, you do not need to master every structure on this list. Instead, focus first on high-quality government bonds, investment-grade corporate bonds, and broadly diversified bond funds or ETFs that spread risk across many issuers.

Which Bonds Might Suit You?

Choosing the right type of bond depends on your goals, time horizon, and risk tolerance.

- Conservative investors: May prefer government bonds, T-bills, high-quality municipal bonds, or investment-grade corporate bonds.

- Income-focused investors: Might use a mix of investment-grade corporate bonds, municipal bonds (for tax-efficient income), and bond funds.

- Aggressive income seekers: Could allocate a modest portion to high-yield or emerging-market bonds, accepting higher risk for potentially higher returns.

Whichever route you choose, bonds should be selected within a broader asset allocation plan that also considers equities, ETFs, and cash holdings. You can revisit Investing in the Stock Market and A Practical Guide to ETFs to see how bonds complement these growth-oriented assets.

How to Invest in Municipal Bonds

Municipal bonds (“munis”) are issued by local governments, such as cities, states, and counties, to finance public projects like schools, roads, hospitals, and water systems. They are generally considered relatively safe, especially when issued by financially sound municipalities.

The key attraction of many municipal bonds is that their interest is tax-exempt at the federal level and sometimes at state or local levels as well. This makes them particularly attractive for investors in higher tax brackets who want to maximize after-tax income.

- How to invest: You can buy individual municipal bonds through a broker or invest via municipal bond mutual funds and ETFs.

- What to check: Credit rating of the issuer, the project being financed, call features, and the tax treatment in your jurisdiction.

Because analyzing the finances of individual cities and states can be complex, many investors prefer diversified muni bond funds managed by professionals.

Risks of Investing in Bonds

Although bonds are often seen as safer than stocks, they still involve several important risks.

Interest Rate Risk

Interest rate risk is the risk that bond prices fall when market interest rates rise. If you need to sell a bond before maturity after rates increase, you may receive less than you originally paid. Longer-maturity bonds are generally more sensitive to rate changes than shorter-term bonds.

Credit (Default) Risk

Credit risk is the possibility that the issuer cannot meet its interest or principal payments. Credit rating agencies such as Moody’s and Standard & Poor’s evaluate issuers and assign ratings that indicate their perceived ability to repay debts. Higher-rated bonds typically offer lower yields, while lower-rated bonds must pay more to compensate investors for higher risk.

Inflation Risk

Inflation risk arises when rising prices erode the purchasing power of the fixed interest payments you receive. Even if you are paid on time, your real (inflation-adjusted) return may be low. Inflation-linked bonds such as TIPS and I-bonds are designed to address this risk.

Liquidity and Reinvestment Risk

Liquidity risk is the risk that you cannot sell a bond quickly at a fair price, especially in stressed markets or for complex structured products. Reinvestment risk occurs when interest rates fall and you must reinvest maturing bonds or coupons at lower yields.

Benefits of Investing in Bonds

Despite these risks, bonds offer several compelling benefits that justify their place in a balanced portfolio.

- Stability: Investment-grade bonds are less volatile than stocks, especially over shorter horizons.

- Income: Regular coupon payments can support living expenses or be reinvested for growth.

- Diversification: Bonds often perform differently from equities, especially during market downturns.

- Visibility of cash flows: Coupons and maturity dates are typically known in advance, making planning easier.

- Priority in bankruptcy: Bondholders are ahead of stockholders in the capital structure if a company fails.

For many investors, a mix of stocks, bonds, and cash delivers a better balance of risk and reward than any single asset class alone.

Where Bonds Fit in Your Investing Journey

Bonds become increasingly important as your investment horizon shortens or your need for portfolio stability grows. Younger investors might hold a smaller percentage in bonds and focus more on growth through equities. As retirement approaches, many gradually increase their bond allocation to reduce volatility and secure income.

By combining bonds with the other vehicles you have learned about in this course—stocks, ETFs, mutual funds, commodities, money markets, and more—you can design a portfolio that aligns with your goals, risk tolerance, and time frame.

Lesson Review Questions

1. What is a bond, and who are the typical issuer and investor?

A bond is a loan agreement in which an issuer, such as a government, municipality, or corporation, borrows money from an investor, who receives regular interest payments (coupons) and the return of principal at maturity.

2. How do bills, notes, and bonds differ in terms of maturity?

Bills are short-term securities with maturities up to about one year, notes are medium-term with maturities of roughly two to ten years, and bonds are long-term securities with maturities longer than ten or twelve years.

3. Why might an investor choose municipal bonds instead of corporate bonds?

Municipal bonds are often considered relatively safe and may pay interest that is exempt from federal and sometimes state or local income taxes, making them attractive for investors seeking tax-efficient income.

4. What are the three primary risks of investing in bonds?

The main risks are interest rate risk (bond prices fall when rates rise), credit risk (the issuer may default on payments), and inflation risk (rising prices erode the real value of fixed coupon payments).

5. How can bonds improve the risk profile of an overall investment portfolio?

Bonds tend to be less volatile than stocks and often behave differently during market stress, providing income, stability, and diversification benefits that can reduce the overall risk of a portfolio.