Exchange-Traded Funds, or ETFs, have become one of the most popular investment vehicles for retail investors. They combine the diversification of mutual funds with the flexibility and low cost of stock trading. For anyone building a long-term wealth strategy, understanding how ETFs work, what they offer, and how to choose the right one is essential to investing literacy.

This lesson explains what ETFs are, how they compare with other pooled investments, why costs matter, and how ETFs can be used to build efficient, diversified portfolios. By the end, you will be able to evaluate whether an ETF aligns with your investment goals, risk tolerance, and time horizon.

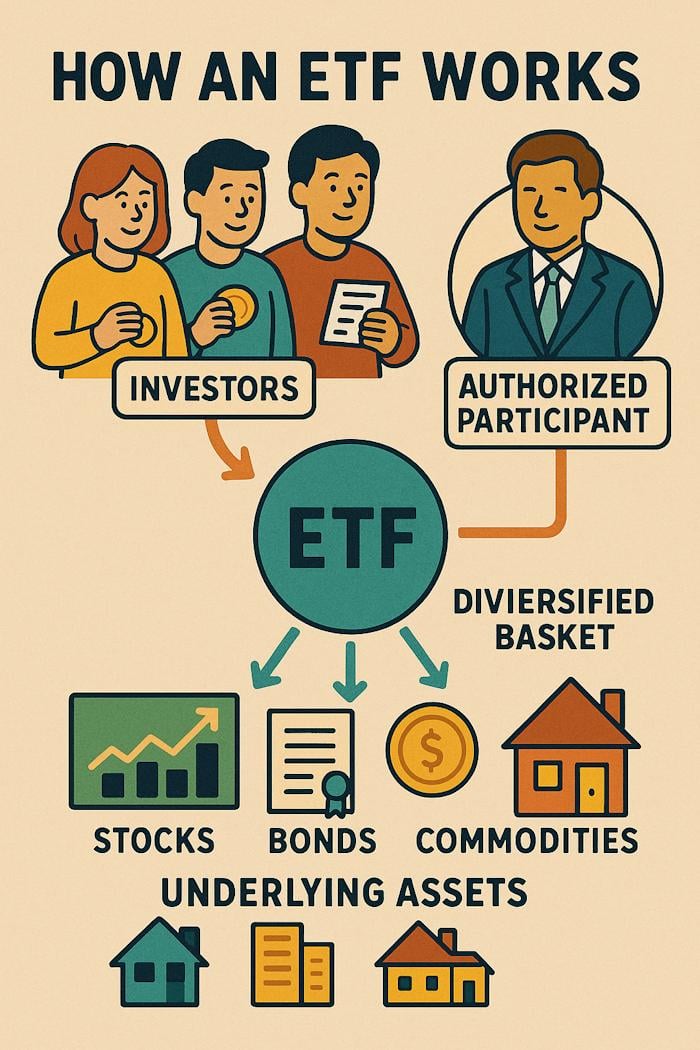

What Is an ETF?

An ETF is a pooled investment fund that trades on a stock exchange just like an individual stock. Investors buy shares of the ETF, and the fund uses that capital to hold a basket of underlying securities—such as stocks, bonds, commodities, or a mix of assets.

Unlike mutual funds, which are only priced and traded once per day, ETFs trade throughout the day at market prices. This intraday liquidity is one of the key features that has made ETFs attractive to both long-term investors and active traders.

Core Characteristics of ETFs

- Diversification – One ETF can give exposure to tens, hundreds, or even thousands of securities.

- Low costs – ETFs generally have lower expense ratios than actively managed mutual funds.

- Intraday trading – ETF prices move throughout the day like stocks.

- Transparency – Many ETFs disclose their holdings daily.

- Tax efficiency – Due to the “in-kind” creation and redemption process, many ETFs generate fewer taxable events than mutual funds.

For new investors, ETFs offer an accessible way to build a diversified portfolio without needing to research and buy dozens of individual stocks.

How ETFs Compare with Mutual Funds and Index Funds

Mutual funds, index funds, and ETFs all allow investors to access diversified baskets of assets. However, their structure and trading mechanics differ.

| Feature | ETFs | Index Funds | Mutual Funds |

|---|---|---|---|

| Trading | Trades all day on exchanges | Bought/sold at end-of-day NAV | Bought/sold at end-of-day NAV |

| Fees | Usually very low | Low | Varies; often higher if actively managed |

| Tax Efficiency | High | Moderate | Low to moderate |

| Minimum Investment | One share | Varies by fund | Varies by fund |

| Intraday Price Movement | Yes | No | No |

Mutual Fund vs. ETF Fees Impact Calculator

See how a high-fee active mutual fund can drain wealth over decades compared with a low-cost ETF or near-zero-fee direct stock investing approach.

Inputs

Results

Formula Used

Mutual Fund/ETF Fees Impact Calculator: The Wealth Drain

Types of ETFs Every Investor Should Know

ETFs come in many forms. Understanding the major categories helps you match an ETF to your strategy and risk tolerance.

1. Equity ETFs

These track baskets of stocks. Some track broad indexes like the S&P 500, while others focus on sectors such as technology, healthcare, or financials. Equity ETFs are the most common choice for long-term investors seeking growth.

2. Bond ETFs

Bond ETFs provide exposure to government, corporate, municipal, or international bonds. They are often used for income generation or portfolio stabilization.

3. Commodity ETFs

These track commodities such as gold, oil, and agricultural products. They can help diversify portfolio risk, but may be more volatile.

4. Sector and Thematic ETFs

Sector ETFs focus on industries, while thematic ETFs invest according to trends such as artificial intelligence, clean energy, robotics, or demographics. These can increase concentration and risk, so they should be used thoughtfully.

5. International and Emerging Market ETFs

These offer global diversification beyond your home market. Emerging markets can offer higher growth potential but entail greater volatility.

6. Leveraged ETFs

A leveraged ETF is an ETF that uses financial instruments, such as futures contracts and options, to amplify the return of its underlying asset. Leveraged ETFs can be risky but can lead to higher profits. Leveraged ETFs are unsuitable for all investors, so it is important to understand the risks before investing.

ETFs are also designed to provide you with built-in leverage. If a fund has the term 2X or 3X in its name, it means it will attempt to replicate the movement of the underlying assets but magnify gains by 2X or 3X.

For example, if you believe the stock market, particularly the S&P 500, will pull back (go down) over the next three months, you may decide to purchase the Rydex 2x Inverse S&P500 ETF (Ticker RSW).

The 2X refers to the ETF managers’ aim to replicate a 2x return based on the price movements of the underlying assets.

So, if the market goes down 5% and you own a 2X Inverse ETF, you should expect to profit by 10%.

If you had a standard 2X ETF that was not inverse and the market went down 5%, you would lose 10%

With all ETFs, the caveat is that they “seek to emulate,” which means it is not always a perfect science, especially with bear-market funds. Some ETFs do the job better than others. Do your research.

7. Inverse ETFs

An inverse ETF is an ETF that tracks the opposite of the underlying asset. For example, if the underlying asset is a stock index, the inverse ETF will track the opposite of the index’s movements. This can be a useful investment strategy for hedging purposes or taking advantage of market corrections. However, it is important to understand the risks before investing in an inverse ETF.

8. Exchange-Traded Notes (ETNs)

The ETN is similar to the ETF in that it trades openly on stock exchanges; however, its underlying characteristics differ. It is a hybrid of an ETF combined with the debt ownership of Bonds.

For example, you may hold an ETN to maturity, and at that point, you will be eligible to receive a cash payment equivalent to the principal value of the note.

Why ETF Costs Matter

One of the biggest advantages of ETFs is their low cost. The expense ratio—expressed as a percentage of your invested assets—reduces returns every year. Over decades, even small cost differences compound significantly.

For example:

- A 0.10% annual fee on a €10,000 investment costs €10 per year.

- A 1.00% fee costs €100 per year.

- Over 20 years, assuming a 6% return, the higher fee fund could reduce your final portfolio value by thousands of euros.

This is why low-cost index ETFs are widely recommended for long-term investors who want broad market exposure without unnecessary fees. For more details on fees and how they erode returns, review our guide on managing investment risk through diversification and asset allocation.

Popular ETFs

Some popular ETFs include:

U.S. Large-Cap / Broad Market ETFs

Small-Cap & Russell ETFs

Dow Jones & Nasdaq ETFs

International Developed Markets

Emerging Markets

Where to buy ETFs?

Some of the best places to buy ETFs include online brokerages like Firstrade, Fidelity, and Charles Schwab, as well as discount brokers like Vanguard and TD Ameritrade. Firstrade offers the broadest number of commission-free ETFs in the industry, so they are well worth investigating.

What is a good strategy for trading ETFs?

A good strategy for trading ETFs is to use dollar-cost averaging over time. This means investing a fixed amount of money in ETFs regularly rather than all at once. This will help reduce the risk of investing in ETFs and allow you to take advantage of price fluctuations over time.

Are ETFs Worth It?

Yes, ETFs offer significant advantages over mutual funds, including diversification, lower costs, higher liquidity, greater flexibility, and more profitable long-term compounding. ETFs should be a core component of your diversified portfolio.

Related Articles:

- ETFs vs. Mutual Funds: The Difference Impacts Your Gains

- The Difference Between ETFs and Mutual Funds is Capital Flow

- ETF Investing Strategy: Beat The Market With MOSES

- ETFs vs. Stocks: 7 Reasons ETFs Are Better Than Stocks

Next Steps in the Course

In the next lesson, we look at hedge funds, REITs, and other alternative investments that play different roles in portfolio construction. Understanding these vehicles will help you see how ETFs compare within the broader investment landscape.

Lesson Review Questions

1. What is an ETF, and how does it differ from a traditional mutual fund?

An ETF is a pooled investment fund that trades on exchanges throughout the day, while mutual funds trade only once at end-of-day net asset value. ETFs typically have lower costs and greater tax efficiency.

2. Why do ETFs tend to be more tax-efficient than mutual funds?

ETFs use an in-kind creation and redemption process that allows the fund to exchange securities with authorized participants instead of selling them, which reduces capital gains distributions.

3. What types of ETFs are suitable for long-term investors seeking growth?

Broad equity ETFs, S&P 500 index ETFs, global equity ETFs, and certain thematic ETFs with long-term growth potential are commonly used for growth-focused portfolios.

4. How do ETF fees impact long-term returns?

Even small differences in expense ratios compound over time. Lower-cost ETFs preserve more of your investment returns, while higher-cost funds reduce portfolio growth over decades.

5. What are some risks of using thematic or sector ETFs?

They concentrate investments in narrow industries or trends, increasing volatility and exposure to sector-specific risks. They should be balanced within a diversified portfolio.

6. What is the expense ratio in ETFs?

An ETF’s expense ratio is the percentage of the fund’s assets used yearly for management and other expenses. This includes management fees, administrative costs, and marketing expenses. The expense ratio can vary from fund to fund but is typically expressed as a percentage of the fund’s assets.

7. Do ETFs pay dividends?

Yes, many ETFs pay dividends, a valuable source of income for investors. Dividends are paid from the fund’s assets and can vary monthly or from fund to fund.

8. Can you day trade ETFs?

Yes, you can day trade ETFs. Day trading ETFs can be profitable, but it’s important to understand the risks involved. Here are a few tips to help you get started:

- Make sure you understand the risks involved in day trading.

- Start small and practice using a demo account before risking real money.

- Choose an ETF that is liquid and has tight spreads.

- Follow your plan, and don’t overtrade!

Please read our full guide to day trading ETFs.

ccc