Money markets are the low-risk, short-term side of investing. While stocks, ETFs, and commodities aim for growth, money market instruments focus on capital preservation and liquidity. They are where investors park cash that may be needed soon, earn modest interest, and reduce overall portfolio volatility.

Understanding money markets is essential for building a solid financial foundation. Your emergency fund, short-term savings, and “dry powder” for future investments will often sit in money market products. Knowing the differences between savings accounts, money market funds, Treasury bills, and certificates of deposit (CDs) helps you choose the right mix of safety, access, and yield.

This lesson explains what money markets are, the main types of money market instruments, how money market funds work, the risks involved, and how to use them effectively in your overall investing strategy.

What Is the Money Market?

The money market is a segment of the financial system where institutions and governments borrow and lend money for short periods, typically from overnight up to one year. It is different from the stock market (equities) and the bond market (longer-term debt). Money market instruments are designed to be very safe, highly liquid, and relatively stable in value.

Common participants in the money market include:

- Banks and credit unions

- Corporations managing cash flow

- Governments issuing short-term debt

- Institutional investors and money market funds

- Individual investors using money market funds or bank products

For everyday investors, “money market investing” usually means using products that invest in this short-term debt — such as money market mutual funds, Treasury bills, or savings products with very low risk.

Key Characteristics of Money Market Investments

Money market instruments share three important traits:

- Safety of principal – They focus on preserving your capital, not chasing high returns.

- High liquidity – Funds can usually be accessed quickly, often within one business day.

- Short maturities – Terms typically range from overnight to 12 months.

Because of these features, money markets are ideal for emergency funds, short-term savings goals, and cash that may soon be deployed into longer-term investments. They are especially relevant when thinking about risk tolerance and time horizon, topics covered earlier in the course in our lessons on setting investment goals and managing financial risk.

Main Types of Money Market Instruments

Although the professional money market includes many technical instruments, individual investors usually encounter a handful of core products. Understanding how each one works helps you choose the right place for your short-term cash.

1. Savings Accounts and Money Market Deposit Accounts

Savings accounts and money market deposit accounts are bank products that pay interest on your balance. They are often insured by government schemes (such as FDIC insurance in the U.S. up to certain limits), making them very low risk.

- Pros: Extremely safe, easy access to cash, simple to understand.

- Cons: Interest rates may be low, especially at traditional banks.

High-yield online savings accounts can offer better rates while maintaining strong safety and liquidity.

2. Certificates of Deposit (CDs) / Term Deposits

A certificate of deposit (CD) is a bank deposit locked in for a fixed term—for example, 3 months, 6 months, or 1 year. In exchange for tying up your money, the bank typically offers a higher interest rate than a regular savings account.

- Pros: Higher interest than regular savings; very low risk when held at insured institutions.

- Cons: Limited access to funds before maturity (early withdrawal penalties).

CDs work well for cash you know you will not need for a specific period, but still want to keep safe.

3. Treasury Bills (T-Bills)

Treasury bills are short-term government debt securities, usually maturing in 4, 13, 26, or 52 weeks. They are sold at a discount to their face value and mature at full value — the difference is your interest.

- Pros: Very low default risk; backed by the national government.

- Cons: Yields may be modest; selling before maturity can lead to gains or losses depending on interest rates.

Because of their safety and short maturities, T-Bills are a core holding in many money market funds.

4. Commercial Paper

Commercial paper is short-term unsecured debt issued by large corporations to finance daily operations such as payroll or inventory.

- Pros: Typically offers higher yields than government bills; very short-term (often under 90 days).

- Cons: Exposed to the credit risk of the issuing company; not normally bought directly by retail investors.

Retail investors rarely buy commercial paper directly. Instead, they gain exposure through diversified money market mutual funds.

5. Repurchase Agreements (Repos)

Repurchase agreements, or “repos,” are short-term loans where one party sells securities (often government bonds) and agrees to buy them back later at a slightly higher price. The difference represents interest.

Repos are widely used by banks and institutional investors to manage cash overnight or for a few days. For individuals, exposure comes indirectly via money market funds.

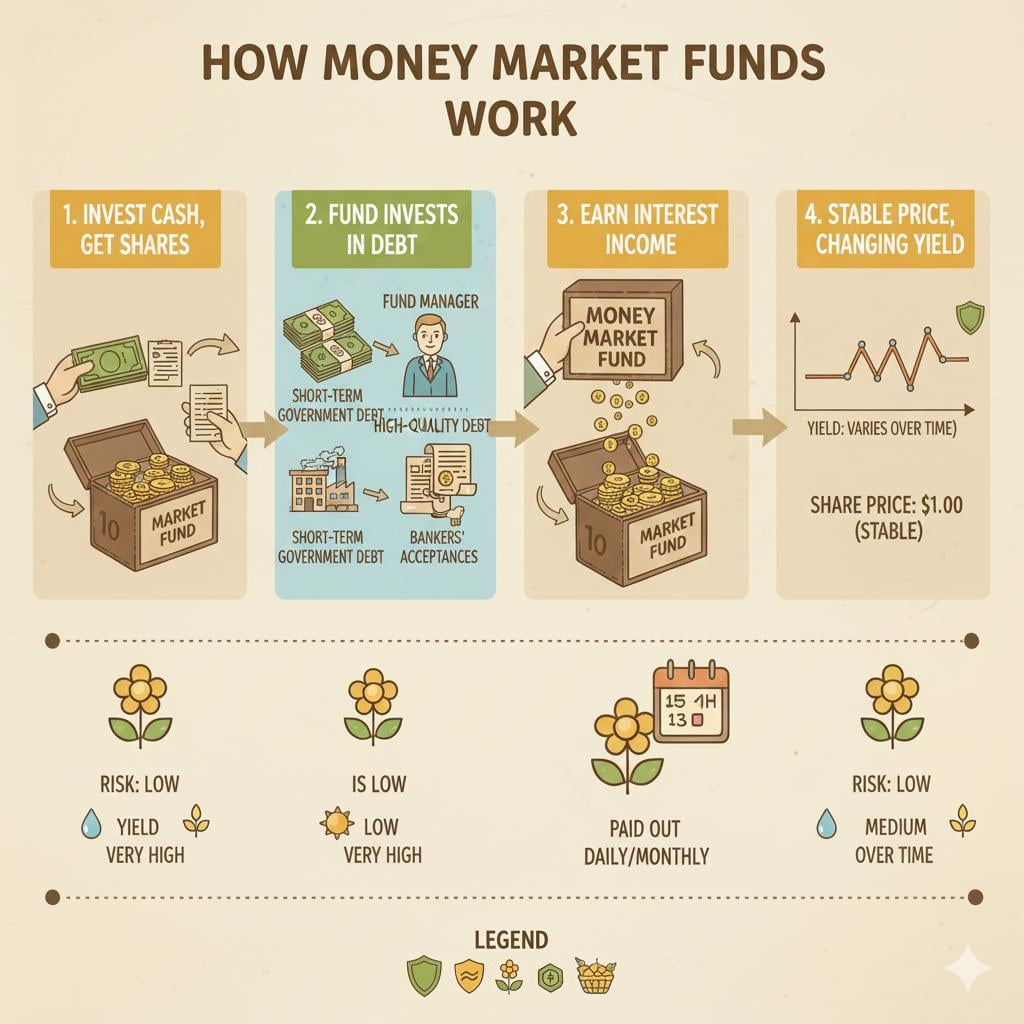

Money Market Mutual Funds

Money market mutual funds are investment funds that pool investor cash and invest it in a diversified portfolio of short-term, high-quality debt instruments such as T-Bills, commercial paper, and repos. Their goals are to maintain a stable value (often targeting a net asset value of 1.00 per share) and to pay investors a modest yield.

How Money Market Funds Work

- You invest cash into the fund and receive shares.

- The fund manager invests in very short-term, high-quality debt instruments.

- As interest is earned, the fund pays out income (often daily or monthly).

- The share price aims to remain stable while the yield changes over time.

Money market funds can be useful for investors who want better yields than a basic savings account while still prioritizing safety and liquidity. However, they are not bank deposits and are not guaranteed; they carry small amounts of credit and interest rate risk.

Benefits of Money Market Investing

Money markets offer several advantages that make them an essential component of a sensible financial plan.

- Capital preservation: Low default risk and stable values.

- Liquidity: Easy access to funds for emergencies or opportunities.

- Reduced volatility: Money market values do not swing like stock prices.

- Flexible use: Ideal for emergency funds, short-term goals, and “parking” cash between investments.

For investors learning to build diversified portfolios, money markets are the foundation on which riskier, higher-return assets like stocks and ETFs can be layered. This links back to earlier lessons in this course on investing in the stock market and ETF investing.

Risks of Money Market Investments

Although money market products are considered low risk, they are not risk-free. Investors should understand the following:

- Inflation risk: Returns may not keep up with inflation, gradually reducing real purchasing power.

- Interest rate risk: Money market yields often fall when central banks cut rates.

- Credit risk: In rare cases, issuers of commercial paper or other instruments can default.

- Fund risk: Money market mutual funds aim to maintain a stable value but are not guaranteed; in extreme conditions, they can “break the buck” and fall below $1 per share.

- Opportunity cost: Keeping too much money in low-yield products can limit long-term growth.

The main trade-off with money markets is safety and liquidity versus growth. Over long periods, equities and balanced portfolios typically deliver higher returns, but money markets play a crucial supporting role in risk management and short-term planning.

True Inflation-Adjusted Purchasing Power Calculator

See how inflation can quietly reduce the real value of your cash, salary, or savings over 5, 10, or 20 years under different inflation scenarios.

Inputs

Results

Formula Used

True Inflation-Adjusted Purchasing Power Calculator Guide

How Money Markets Fit Into Your Investment Plan

Money market investments are not designed to make you wealthy on their own. Instead, they support the rest of your financial plan by providing stability and flexibility.

- Emergency fund: 3–6 months of essential expenses in a high-liquidity money market vehicle.

- Short-term goals: Cash needed within 1–3 years (tuition, house deposit, travel) parked in safer instruments like T-Bills or CDs.

- Rebalancing buffer: Money markets act as a temporary parking spot when buying or selling long-term investments.

- Risk management: Higher cash allocations may be appropriate for conservative investors or during periods of high market uncertainty.

As your investing knowledge grows, you will decide how much of your portfolio to keep in cash and money markets versus growth-oriented assets like stocks, ETFs, or REITs. This ties into asset allocation concepts discussed throughout the course.

Lesson Review Questions

1. What is the primary role of money market investments in a portfolio?

Money markets provide safety, liquidity, and short-term income, making them ideal for emergency funds, short-term goals, and temporary cash holdings.

2. How do Treasury bills differ from certificates of deposit (CDs)?

Treasury bills are short-term government debt sold at a discount and backed by the state, while CDs are bank deposits locked in for a fixed term; both are low risk, but CDs may involve early withdrawal penalties and are issued by banks rather than the government.

3. What are money market mutual funds, and how do they aim to maintain stability?

Money market mutual funds pool investor cash and invest in short-term, high-quality debt like T-Bills and commercial paper. They seek to maintain a stable share price (often $1.00) while distributing interest income.

4. What is the main risk of keeping too much money in low-yield money market products over many years?

The main risk is inflation and opportunity cost: your money may lose purchasing power over time, and you may miss higher returns available from long-term investments like stocks or diversified funds.

5. Why might an investor choose a CD instead of a regular savings account?

An investor might choose a CD because it typically offers a higher interest rate in exchange for locking funds for a fixed term, making it suitable for cash that is not needed immediately.