Before you choose a stock, ETF, or broker, you need one simple thing: a clear reason for investing. Are you trying to retire early, buy a home, live off dividends, or just “beat the market”? Your goals decide everything else: how much risk you take, which assets you choose, and how you react when markets get rough.

This lesson helps you define your investment goals in practical, concrete terms. By the end, you’ll be able to say, “I am investing for this purpose, over this timeframe, and I’m willing to accept this level of risk.” That clarity is the foundation of every serious investing plan.

Savings / Investing Goal Calculator

Calculate how much you need to save each month to reach a financial goal, how long it may take, and how investment returns can accelerate the journey.

Inputs

Results

Formula Used

Advanced Financial Goal Calculator for Saving and Investing

Why Clear Investment Goals Matter

Investing without clear goals is like driving without a destination. You might move fast, but you don’t know if you’re going in the right direction. Clear goals help you:

- Choose suitable investments instead of random “hot tips.”

- Match risk to your real-life needs and personality.

- Ignore marketing hype that promises unrealistic returns.

- Stay invested during normal market ups and downs.

- Measure progress: you know whether you’re on track or need to adjust.

Later in the course, when you learn about stocks, ETFs, funds, and trading strategies, you’ll use these goals as your filter. If a strategy doesn’t support your goals, it doesn’t belong in your portfolio.

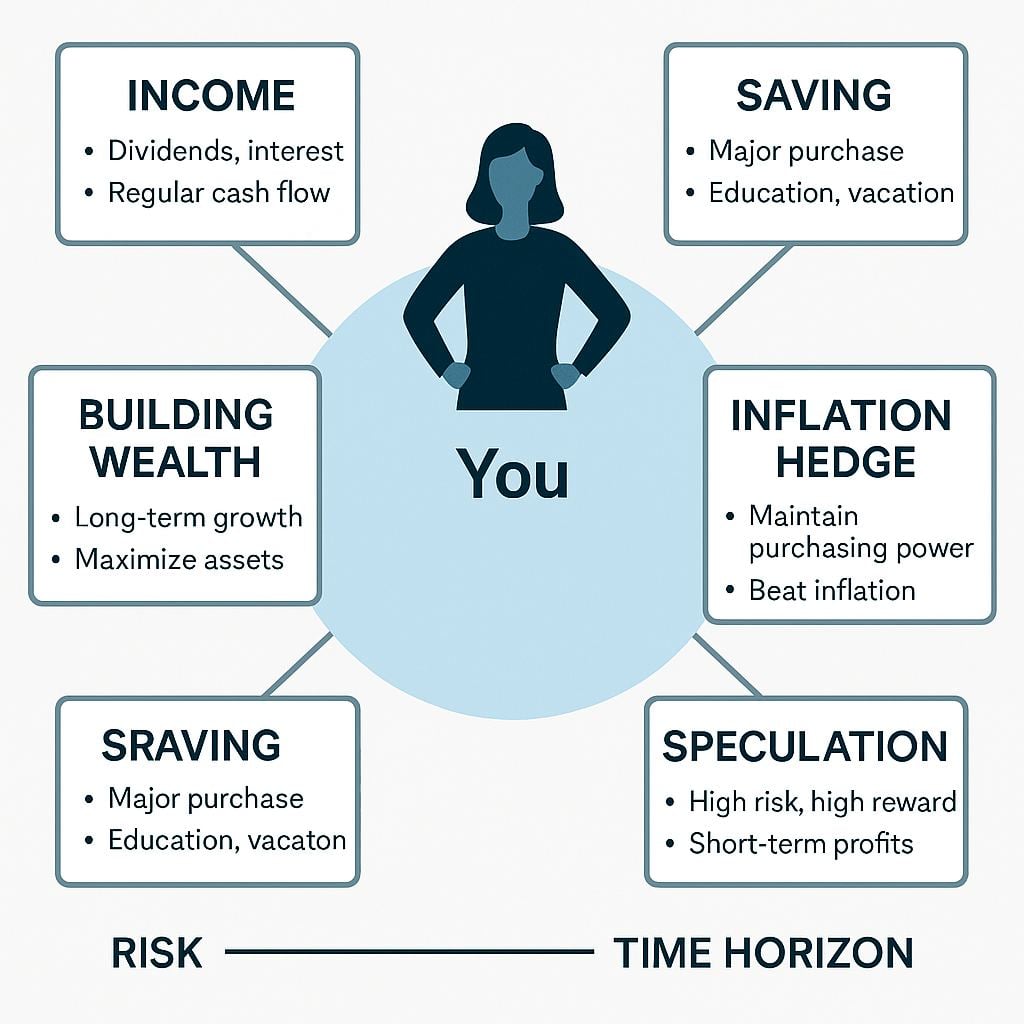

Visual Overview: Core Investment Goals

The Building Blocks of an Investment Goal

A useful investment goal combines four things:

- Purpose – what the money is for (income, retirement, home, freedom, etc.).

- Time horizon – when you need the money (2 years vs. 20 years).

- Risk tolerance – how much volatility and loss you can accept on the way.

- Contribution plan – how much and how often you can invest.

Example: “I want to build a retirement portfolio of €600,000 in 25 years by investing €500 per month into a diversified mix of index ETFs and quality stocks. I can tolerate temporary falls of 20–30% without selling.”

That statement is far more useful than “I want to get rich from stocks.”

The Six Main Types of Investment Goals

Most investors eventually discover that their money is working toward a mix of these six core goals. You might focus on one today and another later in life.

1. Generating Income

Goal: Receive regular cash payments from your investments to support your lifestyle or top up your salary or pension.

Typical investments: dividend-paying stocks, real estate investment trusts (REITs), bond funds, and high-quality individual bonds.

Who this suits: people near or in retirement, or anyone who values steady cash flow and is less focused on maximum long-term growth.

Risks: dividend cuts, interest rate changes, and inflation eroding the real value of your income. Even “income stocks” and REITs can fall sharply in a bear market.

2. Building Wealth (Growth)

Goal: Grow the value of your investments as much as possible over many years, accepting volatility along the way.

Typical investments: growth stocks, broad stock index ETFs, sector ETFs, and equity funds. A classic growth approach is long-term buy-and-hold stock investing.

Who this suits: investors with a long time horizon (10+ years), such as people in their 20s, 30s, or 40s, and anyone who can handle temporary drawdowns of 30–50% without panicking.

Risks: higher short-term volatility and deep bear markets. Over the long term, broad stock markets have historically provided strong returns, but nothing is guaranteed.

3. Saving for Specific Goals

Goal: Build a pot of money for a known future event, such as a house deposit, children’s education, or a major life change.

Typical investments: low-cost index funds or ETFs, high-quality bond funds, and sometimes cash-like instruments for shorter horizons. For longer savings goals, consider index fund investing with regular monthly contributions.

Who this suits: anyone with a clear date and amount in mind, for example, “I need €60,000 in eight years for a house deposit.”

Risks: If you invest too aggressively close to your deadline, a market crash can derail your plans. For goals under three years, keeping money in low-risk vehicles (cash, short-term bonds) is often more appropriate.

4. Hedging Against Inflation

Goal: Protect your purchasing power so your money doesn’t slowly lose value as prices rise.

Typical investments: stocks, real estate, inflation-linked bonds, and sometimes commodities such as gold and other precious metals.

Who this suits: everyone investing for the medium or long term. Inflation quietly erodes cash over decades, so simply staying in a savings account is usually not enough.

Risks: Assets that hedge inflation can still be volatile. Commodities and gold, for example, can go through long periods of underperformance.

5. Retiring Comfortably

Goal: Build a large enough portfolio to support your lifestyle when you stop working, ideally with a safe, sustainable withdrawal rate.

Typical investments: diversified portfolios of stocks and ETFs, plus bonds and possibly real estate. Systems such as the MOSES ETF investing strategy focus on long-term index investing while reducing big crash risks.

Who this suits: almost everyone. Retirement is usually the single biggest financial goal in a person’s life.

Risks: retiring with too little capital, withdrawing too much too early, or holding an overly aggressive portfolio close to or after retirement.

6. Speculating on Future Prices

Goal: Try to profit from short-term or medium-term price moves in stocks, options, futures, crypto, or other instruments.

Typical investments: individual stocks with rapid news-driven moves, leveraged ETFs, options strategies, futures, or forex trading.

Who this suits: experienced traders who understand the risks, use risk management, and are comfortable with the possibility of significant losses.

Risks: very high. Many speculative traders lose money, especially when leverage is involved. For most investors, speculation should be a small “satellite” part of the portfolio, if present at all.

Matching Goals, Time Horizon & Risk

Each goal has a natural time horizon and a sensible range of risk. The table below gives a simple framework; it’s not a rulebook, but a starting point.

| Goal | Typical Time Horizon | Example Investments | Estimated Return Range p.a. (long term) | Risk Level |

|---|---|---|---|---|

| Generate Income | Short to long term | Dividend stocks, REITs, bond funds | 2–6% | Low to medium |

| Build Wealth (Growth) | 10+ years | Growth stocks, stock index ETFs | 7–12% | Medium to high |

| Trading stocks, options, and futures | 3–10 years | Index funds, mixed stock/bond funds | 3–8% | Low to medium |

| Hedge Inflation | 5+ years | Stocks, real estate, inflation-linked bonds | 3–8% | Medium |

| Retirement | 10–40 years | Diversified stock/bond ETF portfolio | 5–9% | Medium |

| Speculation | Days to years | Trading stocks, options, futures | -100% to very high | Very high |

These return ranges are rough, long-term estimates, not promises. Actual results depend on market conditions, costs, taxes, and your behavior.

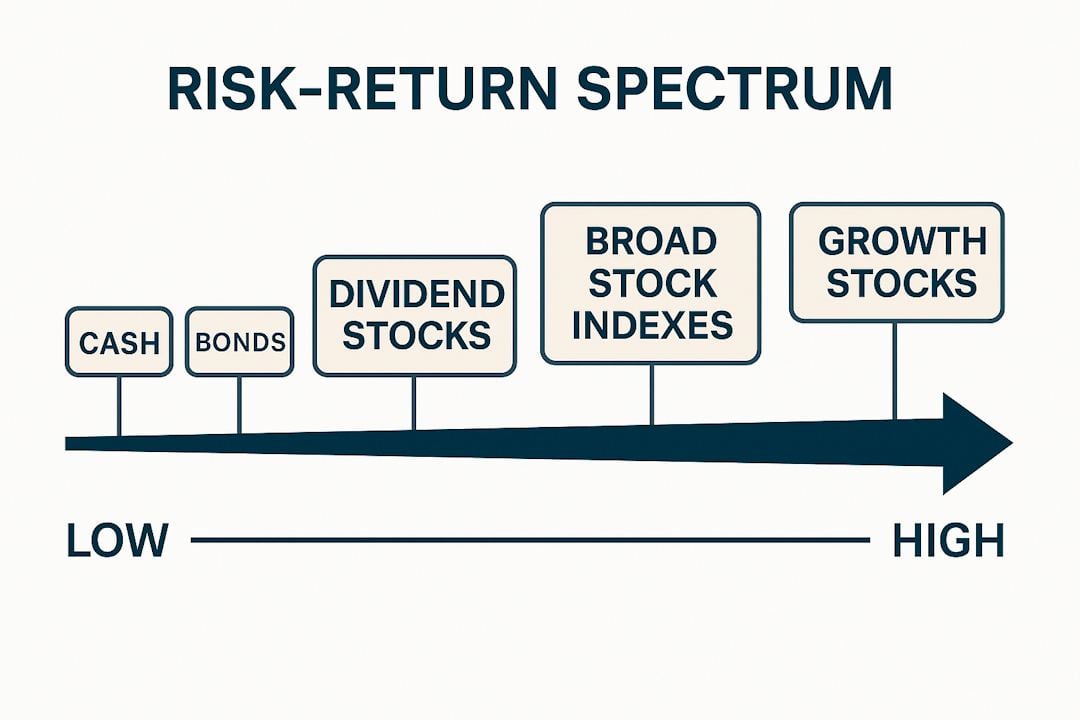

Risk–Return Reality Check: What Is Reasonable?

A useful way to think about returns is to compare yourself to the broad stock market and to world-class investors.

- Broad market (S&P 500): Historically, the U.S. stock market has delivered around 9–11% per year on average over long periods, including dividends.

- Top investors: Legendary investors such as Warren Buffett and George Soros have produced annualized returns of around 20–30% over decades. That is extremely rare and very hard to replicate.

If, over 20+ years, you can achieve returns close to a major stock index while taking sensible risk, you are already doing well. If you manage anything close to 20–25% a year over decades, you are in the territory of the very best.

This is why you should be skeptical of anyone promising “guaranteed 50% returns” or effortless get-rich-quick schemes. Later in the course, we’ll look at how to recognize and avoid common stock market scams.

From Goal to Plan: A Simple 5-Step Process

Here is a straightforward way to turn your goals into an investing plan.

- Write down your main goals. For example: “Retirement at 65”, “€40,000 for a home deposit in 8 years”, “€300 per month in dividend income.”

- Assign a time horizon to each goal. Short term (0–3 years), medium term (3–10 years), long term (10+ years).

- Choose a risk level. Be honest. How would you feel if your portfolio dropped 30% this year? If the answer is “I’d sell everything,” reduce your risk.

- Pick a rough asset mix. For example:

- Short-term goals: mostly cash and short-term bonds.

- Medium-term goals: a mix of stock and bond funds.

- Long-term goals: more in stocks and equity ETFs for growth.

- Automate contributions and review yearly. Set up monthly investments where possible. Once a year, check whether your portfolio still matches your goals and risk tolerance. Articles like how to manage a stock portfolio and crafting a diversified portfolio can help refine this.

Over time, some goals will be met and disappear, new ones will appear, and your risk tolerance will change. The process is ongoing, but the structure stays the same.

How This Lesson Fits into Course 101

In Lesson 101-01, you looked at different types of investors. This lesson adds the next layer: your personal goals. Together, your investor type and your goals form the “compass” you use for the rest of the course.

In the upcoming lessons, you’ll learn about market history, risk management, and specific vehicles such as stocks, mutual funds, and ETFs. As you read them, continually ask:

- “Which of my goals does this investment type support?”

- “Is the risk level appropriate for my time horizon?”

- “What role could this play in my overall plan?”

That habit will keep you grounded when markets, headlines, and social media try to pull you in every direction at once.

Lesson Review Questions

1. What are the four key elements of a well-defined investment goal?

A solid investment goal combines a clear purpose (what the money is for), a time horizon (when you need it), your risk tolerance (how much volatility you can endure), and a contribution plan (how much and how often you will invest).

2. How does investing for income differ from investing for growth?

Income investing focuses on regular cash payments from dividends, interest, or rents and tends to favor more mature, stable assets. Growth investing focuses on increasing the value of your capital over time, usually through stocks and equity funds, and accepts higher volatility and fewer immediate cash payouts.

3. Why is the time horizon so important when choosing investments for a specific goal?

The shorter your time horizon, the less time you have to recover from market falls. For goals within a few years, high-risk assets like stocks can be dangerous because a crash might hit right before you need the money. For long-term goals, you can usually accept more volatility and use higher-growth assets like stocks and index ETFs.

4. What makes speculative trading unsuitable as a core strategy for most investors?

Speculative trading often involves high leverage, rapid decisions, and large potential losses. Many traders lose money, especially without strict risk management. Because the downside is so large and unpredictable, speculation is usually better kept as a small side activity, not the foundation of a long-term wealth or retirement plan.

5. If your main goal is retirement in 25 years, what broad mix of assets might be more suitable, and why?

For a 25-year retirement goal, a portfolio tilted toward stocks and stock index ETFs, with some bonds for stability, is often more suitable. The long horizon allows you to ride out short-term volatility, benefit from stock market growth, and then gradually reduce risk as retirement approaches.

6. How can you use your goals to avoid falling for “get rich quick” promises?

When you know your realistic long-term goals and understand typical return ranges, you can immediately question any offer that promises huge, guaranteed profits with little risk. Instead of chasing hype, you can check whether a strategy genuinely fits your time horizon, risk tolerance, and written plan—and if it doesn’t, you can confidently ignore it.